Urea Volatility Pushes DEF Prices Higher as Global Supply Tightens

Although fuel prices have been the focus of headlines, DEF prices are just as volatile. The shift is being driven by rapid changes in the global urea market, where disruptions tied to Middle East tensions are tightening supply and accelerating cost increases.

At a global level, urea supply is highly concentrated. The Gulf region accounts for a large share of seaborne exports, and most of that volume typically moves through the Strait of Hormuz. Recent escalations, including force majeure declarations, damage to natural gas infrastructure, and severe shipping constraints, have reduced available supply and made trade flows less reliable. With no strategic reserves to absorb the shock, prices are adjusting quickly and in large increments.

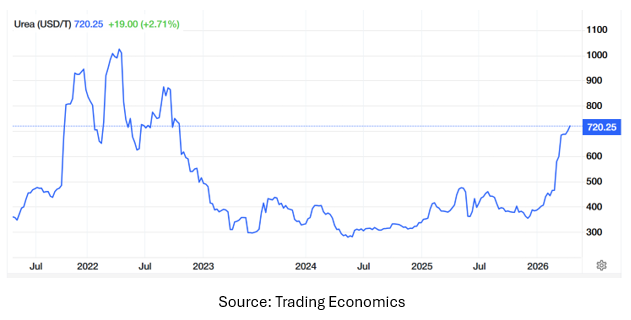

Those global pressures are showing up clearly in benchmark pricing. In the U.S., the New Orleans (NOLA) market has moved sharply higher. Prices have climbed into the $700+ per ton range in the past weeks, up significantly from earlier levels in the $400s. Globally, some spot values have pushed even higher, reflecting how tight the market has become.

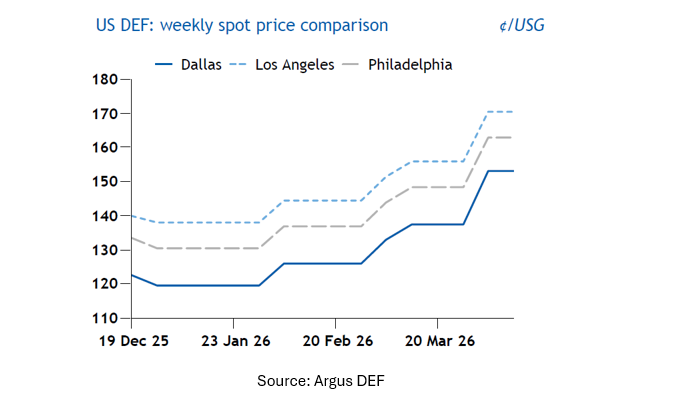

In North America, however, the situation is more nuanced. DEF supply remains stable overall, supported by strong domestic urea production and limited reliance on imports from the Middle East. But that does not mean the market is unaffected. Pricing is still being pulled higher by global dynamics, and recent data shows that domestic DEF values have already moved up meaningfully. According to the latest Argus data, U.S. bulk DEF prices increased by roughly 15–20¢/gallon across major markets in early April.

Demand is also reinforcing the trend. In North America, DEF consumption is closely tied to diesel usage, and that demand is strengthening. Trucking activity has picked up, with freight volumes reaching their highest levels in several years, while diesel demand remains steady above 4 million barrels per day. At the same time, seasonal agricultural activity is ramping up. Fertilizer applications and early planting in the Midwest are increasing both diesel and DEF consumption, tightening regional balances.

Because DEF is made with 32.5% urea, rising urea costs continue to be the primary driver behind higher DEF prices. What stands out in the current environment is not just the direction of prices, but the speed and frequency of change. The market is now adjusting more dynamically, creating challenges for both suppliers and buyers. DEF prices are no longer moving in predictable cycles. Adjustments that once took weeks are now happening within days, and in some cases, multiple times in a single week.

Looking ahead, the North American DEF market remains well supplied, but it is not insulated from global pricing forces. As long as urea markets stay tight and global trade flows remain disrupted, upward pressure on DEF pricing is expected to continue, even without a direct supply shortage in the U.S.

For now, the takeaway is clear: availability is holding steady, but pricing is being driven by a global market that is moving faster than usual, and that pressure is unlikely to ease in the near term.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")