Week in Review – Oil Eases on Iran Talks, But Supply Recovery Could Take Years

Energy markets are ending the week with a noticeable shift in direction, but the underlying risks tied to the Iran conflict remain. This morning, WTI crude opened down more than $3.50 per barrel and is set to finish the week lower by over $5, as the U.S. and Iran continue negotiations and signal progress toward a deal. President Trump indicated that Iran has agreed to terms it had previously resisted, raising expectations that a broader agreement could be reached soon. At the same time, a parallel 10-day ceasefire between Israel and Hezbollah is helping calm regional tensions. Iran has also stated that the Strait of Hormuz is open during the truce, which immediately pressured crude prices lower – triggering an estimated 9% decline – as markets reacted to the possibility of restored oil flows through one of the world’s most critical shipping lanes.

But the reality on the water tells a more complicated story. Despite headlines suggesting the Strait is “open,” the U.S. naval blockade remains fully in force for Iran-related shipping, and traffic through the region is still extremely constrained. U.S. forces have reportedly turned back multiple vessels, while only a limited number of tankers, some linked to China, have managed to exit the strait. Others are beginning to reroute entirely, including shipments moving from Saudi Arabia into the Red Sea, marking one of the first alternative flows since the blockade began. European nations, including the UK and France, are now considering coordinated naval efforts to secure safe passage, underscoring the fragility of global supply chains even as diplomatic progress unfolds.

At the same time, longer-term supply risks are coming into sharper focus. According to International Energy Agency chief Fatih Birol, it could take up to two years to restore a meaningful share of oil and gas production lost in the Iran war. That timeline challenges the market’s current assumption that supply disruptions are temporary. Damage to oil fields, refineries, pipelines, and LNG infrastructure across the Persian Gulf has already removed millions of barrels per day from the market, with more than 80 facilities impacted.

The scale of disruption is significant. Earlier estimates suggest as much as 13 million barrels per day of oil production has been knocked offline, with total export losses even higher when refined products are included. Natural gas recovery could lag further, with some LNG terminals requiring more than two years to return to normal operations. In the physical market, this is already showing up in tighter supply, stronger spot pricing, and increased competition among refiners, particularly in Europe and Asia, where some are beginning to cut runs due to limited feedstock availability.

Demand is also starting to respond. Early signs of demand damage are emerging, including fuel rationing, reduced industrial activity, and rising inflation pressures in energy-importing economies. These effects are expected to hit emerging markets hardest, especially across Asia and Africa, where reliance on imported energy is high, and price sensitivity is more immediate.

For fuel buyers, the takeaway is clear: the market is easing on sentiment, not on structure. Even with progress toward a deal, the physical damage across the region suggests that tightness in global energy markets could persist well beyond the end of active conflict.

Prices in Review

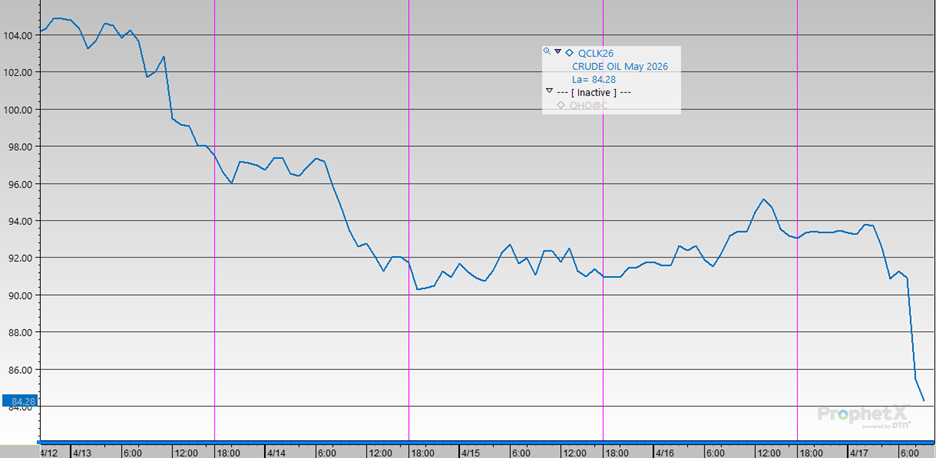

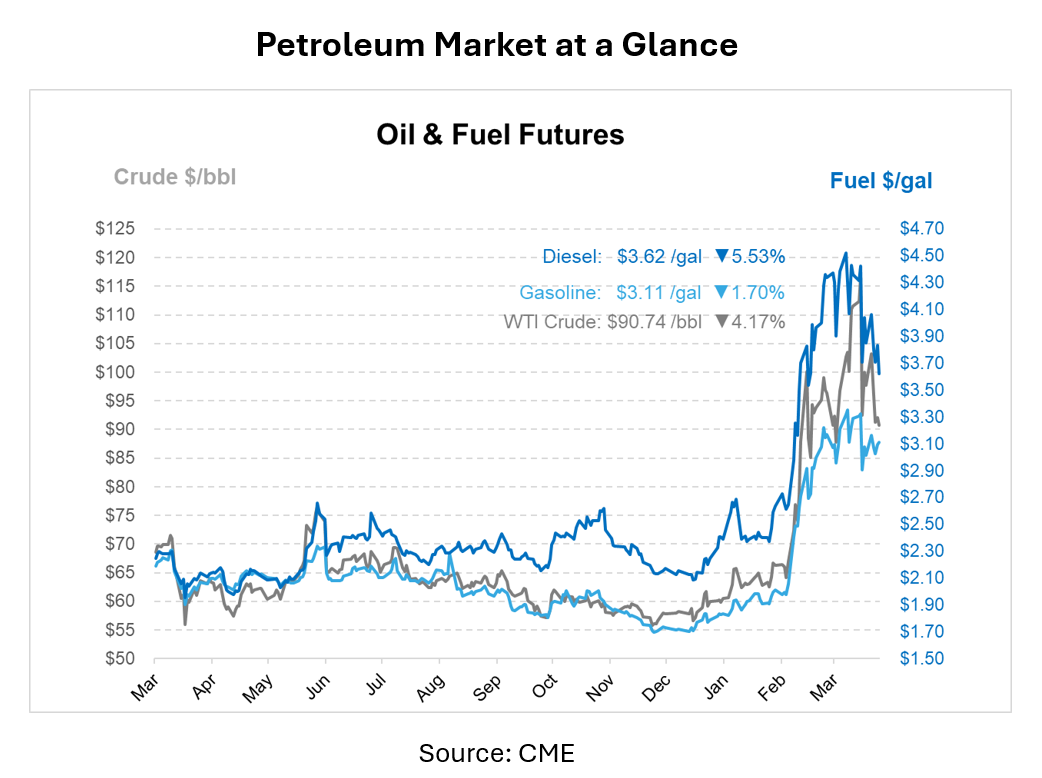

Crude prices moved lower through most of the week before a modest recovery at the end. Prices opened at $102.00 on Monday, declined to $97.99 on Tuesday, and then dropped further to $92.02 on Wednesday. The market opened slightly lower at $91.47 on Thursday, then rebounded to $93.18 on Friday. From Monday to Friday, crude prices decreased by $8.82 per barrel, representing an overall 8.6% decline.

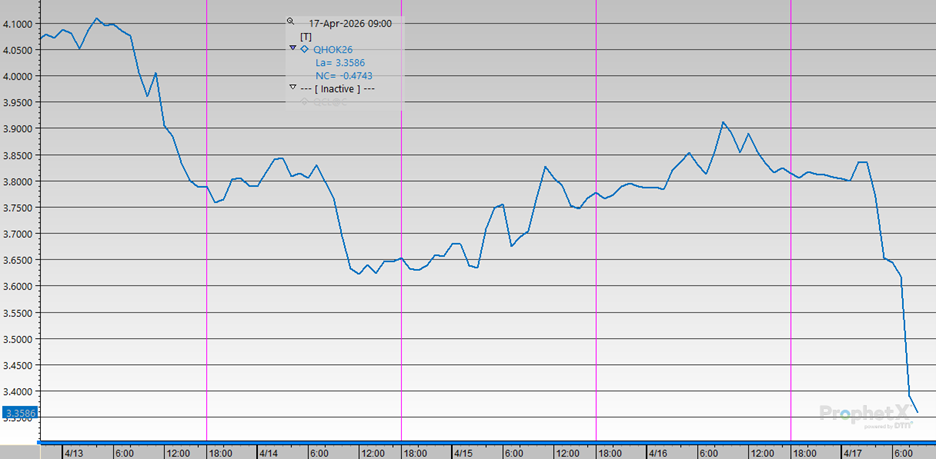

On Monday, Diesel prices opened at $4.0200, then declined to $3.7770 on Tuesday and to $3.6778 on Wednesday, the lowest level of the week. The market recovered to $3.7834 on Thursday. Throughout the week, diesel prices decreased by $0.2366 per gallon, representing a 5.9% decline.

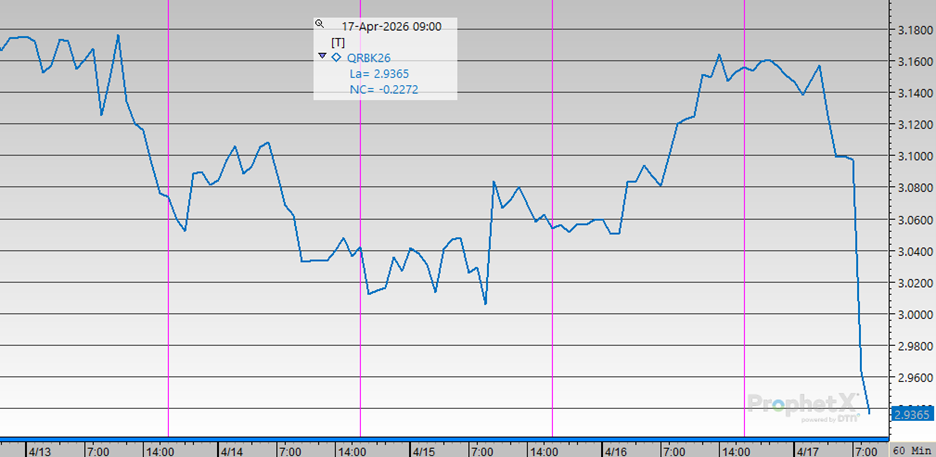

Gasoline prices opened at $3.1100 on Monday and slipped to $3.0939 on Tuesday, then reached $3.0387 on Wednesday. Momentum shifted later in the week, with prices rising to $3.0627 on Thursday and falling to $2.9635 on Friday, the lowest level of the week. Overall, gasoline prices decreased by $0.1465 per gallon, representing an approximate 4.7% decline during the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")