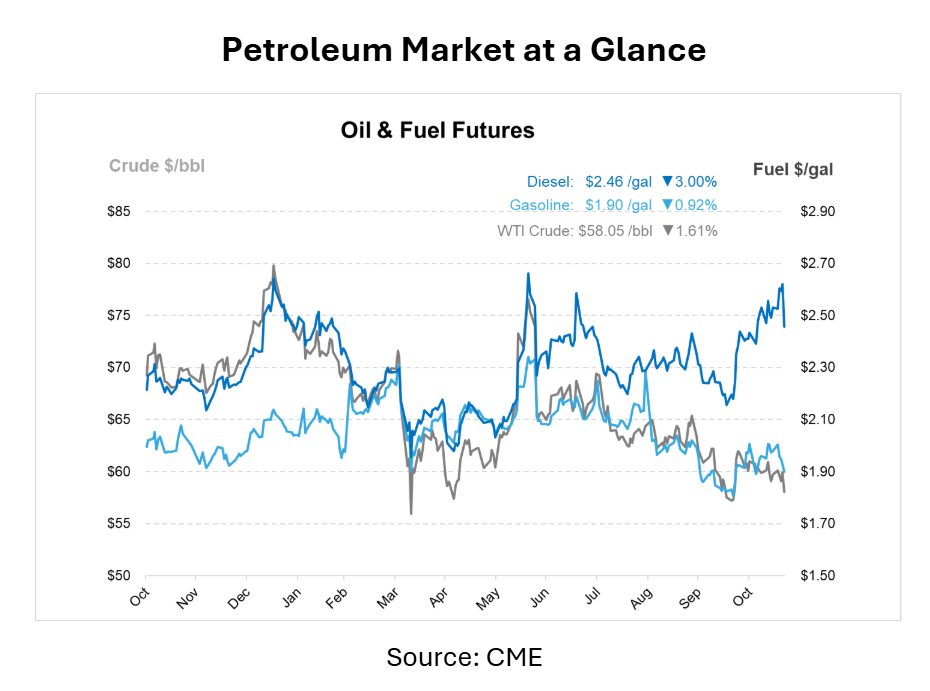

Week in Review – Prices End the Week Lower on Peace Plan Headlines, Inventory Swings, and Pipeline Outages

Crude markets were pulled lower this week as markets balanced evolving geopolitical risks, shifting supply expectations, and mixed economic signals. After a midweek price increase driven by stronger U.S. crude inventory draws and a global equity rally, prices resumed their decline. Brent fell back to the low $62/bbl range while WTI slipped below $59/bbl, placing both benchmarks on track for weekly losses exceeding 2%. The primary drag on sentiment came from renewed diplomatic movement between the U.S., Russia, and Ukraine. Washington has drafted a framework for a potential peace plan, and Ukrainian President Volodymyr Zelenskiy said he would work with the U.S. on negotiations. Initially, the talks were viewed as reducing the risk of sanctions tightening Russian supply, though an actual agreement remains far from certain. At the same time, U.S. sanctions on Rosneft and Lukoil took effect Friday, with Lukoil facing a December 13 deadline to restructure or divest its large international portfolio.

Outside of diplomatic efforts, military tensions continued to shape risk sentiment. Ukraine carried out overnight strikes on Russia’s Ryazan and Ilsky refineries, proving that the conflict remains highly active despite talk of a peace framework. India added another wrinkle to global flows, reporting a nearly 9% increase in crude imports in October, which is its highest level in six months. Meanwhile, one major Indian refiner simultaneously stopped purchasing Russian crude in compliance with sanctions. Meanwhile, ICE Futures Europe introduced tighter rules that would ban diesel imports if the producing refinery had processed Russian crude within the 60 days preceding loading, adding further uncertainty to downstream product flows.

On the domestic front, crude inventories fell sharply by 3.4 million barrels, reflecting strong refining runs, improved margins, and firm export demand. However, gasoline and diesel inventories posted their first build in over a month, signaling softer fuel consumption heading into late November. Market expectations for a December Federal Reserve rate cut fell sharply, from 90% a month ago to just 35%, contributing to a stronger U.S. dollar and pressuring oil prices by making dollar-denominated commodities more expensive for global buyers.

Adding to domestic supply concerns, the 400-mile Olympic Pipeline system, which is critical for moving gasoline, diesel, and jet fuel from northern Washington to Oregon, remained shut for most of the week following a leak detected on November 11. The outage prompted Washington’s governor to declare a state of emergency, as jet fuel deliveries to Seattle-Tacoma International Airport were disrupted. The pipeline operator continues 24-hour excavation and inspection operations, but has not yet provided a timeline for full restart.

Prices in Review

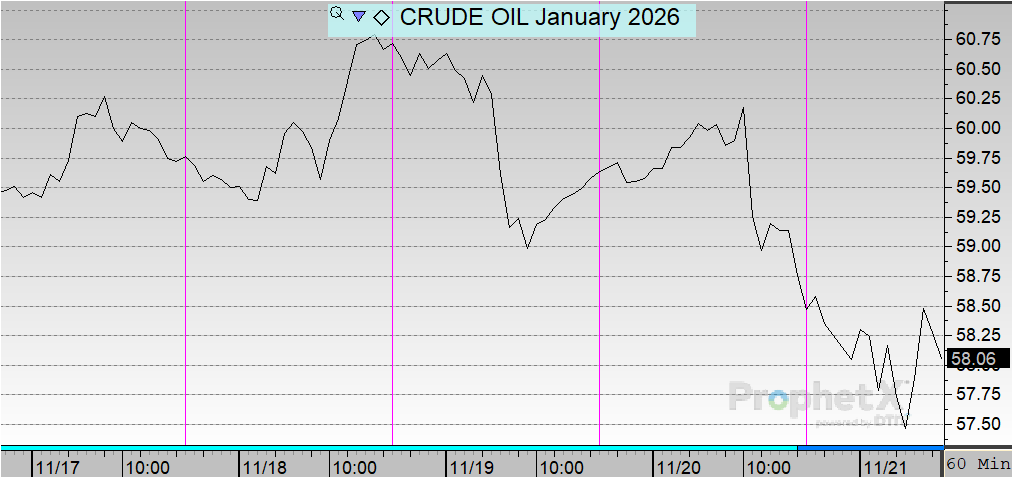

Crude prices opened at $59.80 on Monday and held relatively steady early in the week, dipping slightly to $59.74 on Tuesday. The market saw its strongest upward movement on Wednesday, when prices briefly climbed to $60.62, the weekly high. Momentum faded again on Thursday as crude slipped to $59.63, followed by a sharper decline on Friday with an opening price of $58.80, the weekly low. Overall, crude fell $1.00, representing a 1.67% decrease for the week.

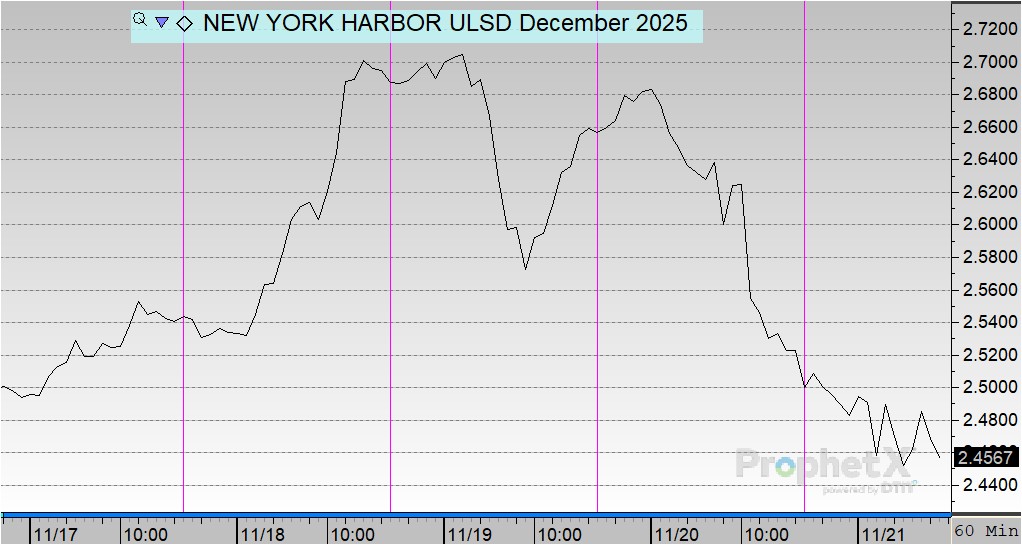

Diesel opened the week at $2.5217 on Monday and showed modest increases, rising to $2.5382 on Tuesday. Prices surged midweek, reaching the weekly high of $2.6892 on Wednesday, marking the sharpest upward move of the week. After that spike, diesel edged lower to $2.6568 on Thursday, before retreating further on Friday with an opening price of $2.5227, nearly unchanged from Monday’s level. Overall, diesel prices increased by just $0.0010, reflecting a 0.04% gain for the week.

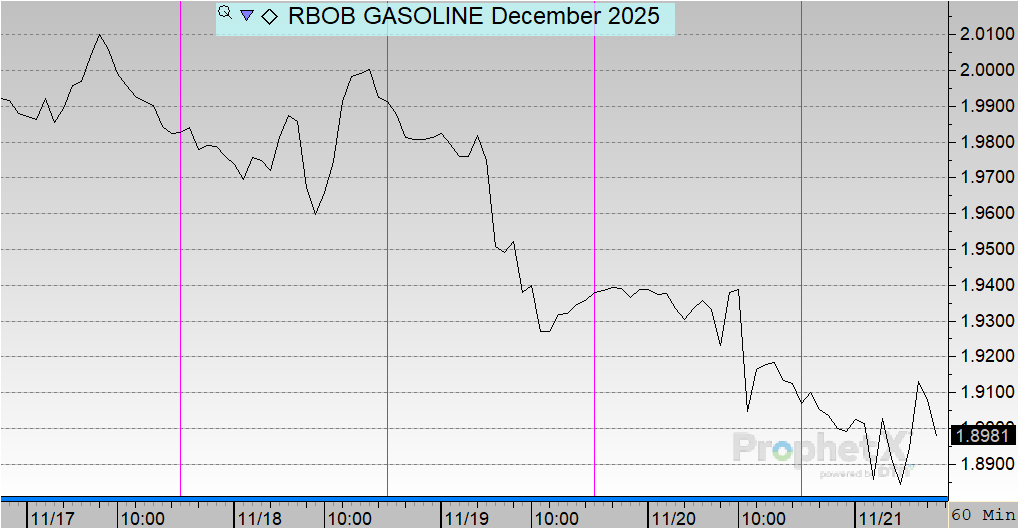

Gasoline prices opened at $2.0077 on Monday and trended lower through most of the week. The sharpest decline came on Tuesday, when prices fell to $1.9835, followed by a slight jump to $1.9940 on Wednesday. The downward momentum returned on Thursday as gasoline slipped to $1.9378, before reaching the weekly low of $1.9135 on Friday. Overall, gasoline fell $0.0942, marking a 4.69% decrease for the week.

This article is part of Week in Review

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")