Crude Pulls Back, but Inventory Declines Keep Market Tight

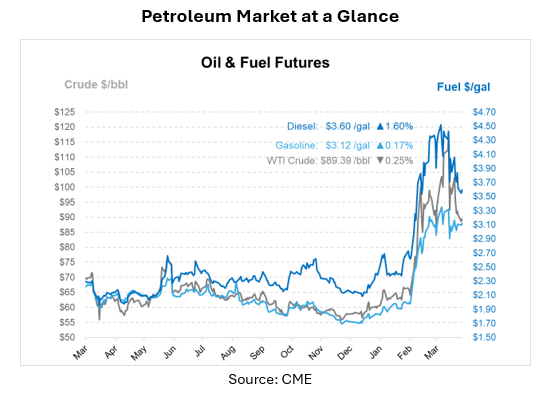

Oil prices are pulling back slightly, but the market remains under pressure. This morning, Brent crude traded near $95 per barrel, while prompt WTI hovered around $89, as the market weighs the possibility of last-minute U.S.–Iran talks against the risk of renewed escalation. The ceasefire is set to expire soon, and with the Strait of Hormuz still largely blockaded, a significant share of global oil flows remains disrupted, keeping uncertainty high. President Donald Trump has indicated he does not want an extension, while Iranian officials have yet to confirm participation in talks and continue to reject negotiations under pressure.

On the supply side, disruptions continue to stack up across multiple regions. Russia has been forced to reduce oil output by an estimated 300,000 to 400,000 barrels per day due to ongoing attacks on ports and refineries, including damage near key export infrastructure in the Black Sea. Additional constraints are coming through pipeline systems, with flows along the Druzhba network facing interruptions and changes in routing. At the same time, global crude flows are shifting rapidly. Shipments from West Texas to Gulf Coast export terminals reached a record 5.27 million barrels per day last week, with some pipelines operating above capacity as U.S. barrels are pulled into international markets.

Even with that surge, it’s not enough to rebalance the system. U.S. crude exports are on track to exceed 5.4 million barrels per day in April and May, with a significant portion heading to Asia, where supply shortages are most acute. But the loss of Middle Eastern barrels due to the Hormuz disruption is far larger – total seaborne exports to Asia have dropped by roughly 10 million barrels per day compared to pre-war levels. Refined product flows show a similar gap, with exports through the Strait effectively collapsing. The result is a global market that is scrambling to re-route supply but still coming up short.

Inventory data reinforces that tightening trend. Global crude and product stocks are already drawing down and could fall by as much as 900 million barrels even if a ceasefire is extended and flows begin to normalize by early summer. If disruptions persist for another month or more, total inventory losses could climb well above 1 billion barrels, pushing global stockpiles toward multi-year lows. In that scenario, price forecasts move meaningfully higher, with some projections pointing to triple-digit Brent prices in the near term.

At the same time, demand-side pressure is beginning to emerge. Higher fuel and food costs are expected to weigh on consumer spending, particularly among lower-income households. Growth in real disposable income is projected to slow, and consumption forecasts are being revised lower in more adverse pricing scenarios. This creates a more complex market dynamic, with a tight supply supporting prices, but economic strain is beginning to test demand resilience.

Governments are starting to respond to the impact on the consumer level. In Canada, Prime Minister Mark Carney announced a temporary suspension of the federal fuel excise tax on gasoline and diesel from April 20 through September 7, 2026. The measure is expected to lower prices by about 10 cents per litre for gasoline and 4 cents for diesel, offering immediate relief for consumers and key industries like trucking, agriculture, construction, and delivery. The policy also extends to aviation fuels and is part of a broader effort to reduce operating costs and support economic activity while global energy markets remain under pressure.

China is also responding from a different angle, lowering retail gasoline and diesel price caps for the first time this year, signaling an effort to manage domestic fuel costs amid elevated global prices. Meanwhile, European officials are warning that even under a best-case scenario, fuel shortages could create a challenging summer, particularly if flows through the Strait of Hormuz are not fully restored.

All of this leaves the market in a fragile balance. Short-term price direction is being driven by headlines around negotiations and ceasefire expectations, but the underlying fundamentals remain tight. Supply disruptions are widespread, inventories are falling, and replacement barrels are not keeping pace with losses.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")