North American Rig Counts Decline While Crude Oil Prices Climb the Ladder

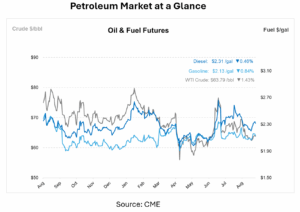

North American rig activity ticked lower last week, underscoring the market’s push-pull between fundamentals and geopolitically driven supply risk. After a fourth straight gain on Monday, WTI is back down this morning by over $1 to $63/bbl, and October Brent is sitting at $67/bbl. The immediate catalyst for the decline was Ukraine’s weekend drone strikes on Russian energy infrastructure, dimming prospects for a ceasefire and raising the odds of fresh U.S. sanctions that could further curb Russian exports.

Russia has been heavily reliant on distillate exports lately. With ongoing tightness in U.S. inventories, which sit about 15% below their five-year average, diesel prices have been on a steady incline for a few weeks. Gasoline has also eased (October RBOB slightly lower), reflecting softer demand signals and localized Russian gasoline shortages after infrastructure disruptions. Russia also plans to cut naphtha exports following a fire at its Ust-Luga complex, reinforcing concerns across the light-ends slate.

U.S. and Russian officials reportedly discussed potential energy deals on the sidelines of Alaska talks, even as President Trump renewed threats of sanctions absent progress toward peace within two weeks. Trade frictions are another headwind. A draft U.S. plan would impose tariffs up to 50% on Indian exports, and separate pressure on New Delhi’s Russian crude purchases has Indian refiners signaling October buys of 1.4–1.6 Mbpd versus the beginning of the year’s 1.8 Mbpd average. Upstream, Alberta is exploring an investment in Japanese refining to enable more processing of the province’s heavy crude, which is another sign of shifting global crude flows.

North America’s rig count fell by 718 (U.S. 538; Canada 180). The U.S. tally includes 411 oil and 122 gas rigs. Year over year, North America is down 86 rigs. Despite the decrease, U.S. crude production remains near records at approximately 13.38 Mbpd. The EIA nonetheless cut price forecasts, seeing Brent averaging around $58/bbl in the latter part of the year and WTI around $54, with 2026 WTI near $47.77. These forecasts are below the $64 breakeven many US officials cite and well under the $83 typically needed to spur a robust drilling ramp.

In regulatory news, the EPA moved to partially block California’s proposed State Implementation Plan revisions around heavy-duty truck inspection and maintenance, opening a 30-day comment window. With tariffs moving from hypothetical to operational and capex decisions buffeted by tax provisions and uncertain demand, crude is expected to remain between $65–$74 while volatility stays elevated.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")