Week in Review – Oil Markets Remain Caught Between Diplomacy and Escalation

Oil markets are closing higher as concerns around the Strait of Hormuz continue to dominate global energy markets. WTI futures traded up more than $3/bbl this morning and are now on track to finish the week up over $9/bbl week-over-week, while Brent crude moved back above $108/bbl. The latest move comes as hopes for a quick diplomatic resolution between the U.S. and Iran continue to fade, keeping the market focused on the risk of prolonged disruptions to one of the world’s most important energy corridors.

President Trump stated that his patience with Iran was “running thin” following meetings with Chinese President Xi Jinping in Beijing. Trump said both leaders agreed that Iran cannot be allowed to possess a nuclear weapon and that the Strait of Hormuz must reopen. At the same time, Iran’s foreign minister said Tehran is prepared both for diplomacy and for a return to fighting, reinforcing concerns that tensions in the region could continue for weeks or even months. Reuters reported that comments from both sides further damaged confidence in a near-term peace agreement, helping push oil prices higher throughout Friday’s session.

Even though some vessels have slowly started moving through the Strait again, shipping activity remains far below normal levels. Before the conflict, roughly 140 vessels per day typically moved through the waterway. Recent reports suggest traffic has improved modestly, but volumes remain dramatically reduced.

Markets are also watching the physical supply picture become increasingly tighter. According to Goldman Sachs Research, U.S. gasoline inventories have been drawing at an aggressive pace since April, with inventories now sitting roughly 5% below their historical seasonal median. Analysts pointed out strong export demand, resilient domestic consumption, and refiners shifting yields toward distillates as key drivers behind the tightening gasoline market. At the same time, the International Energy Agency estimated a global oil deficit of 5.3 million barrels per day during April, showing how strained balances have become since the onset of the Iran conflict.

Another major development this week came from U.S. Strategic Petroleum Reserve flows. Reports indicated that nearly half of the crude oil released from the SPR is now being exported overseas rather than remaining in domestic markets. That trend is being viewed by many traders as a signal that global supply conditions are significantly tighter than they appear on paper, especially as buyers across Europe and Asia continue searching for replacement barrels amid shipping disruptions in the Persian Gulf.

Outside the Middle East, Ukraine’s continued attacks on Russian refining infrastructure are adding another layer of risk to global energy balances. Reuters reported that Ukrainian drone strikes have curtailed roughly 700,000 barrels per day of Russian refining capacity between January and May across 16 different refineries. Earlier today, Ukraine reportedly targeted Russia’s Ryazan refinery, one of the country’s largest facilities, with a throughput capacity of roughly 340,000 barrels per day. The attacks are contributing to growing concerns about diesel and refined product availability globally, particularly as inventories were already relatively tight before the conflict escalated.

Meanwhile, several countries are now actively working to reduce their dependence on the Strait of Hormuz altogether. The UAE announced it is accelerating construction of a new pipeline project that would significantly expand export capacity through Fujairah by 2027, allowing more crude exports to bypass the Strait entirely. President Trump also said discussions with China included the possibility of China purchasing more U.S. crude oil, particularly from Alaska and Gulf Coast exports, as buyers look for more stable supply options outside the Persian Gulf.

The market continues to show just how sensitive prices remain to developments in the war. Every headline tied to the Strait of Hormuz, refinery outages, sanctions, or diplomatic negotiations has the potential to move crude prices sharply within hours. With diesel and gasoline inventories tightening globally and shipping disruptions still limiting flows through the Gulf, volatility is likely to remain elevated heading into the summer driving season.

Prices in Review

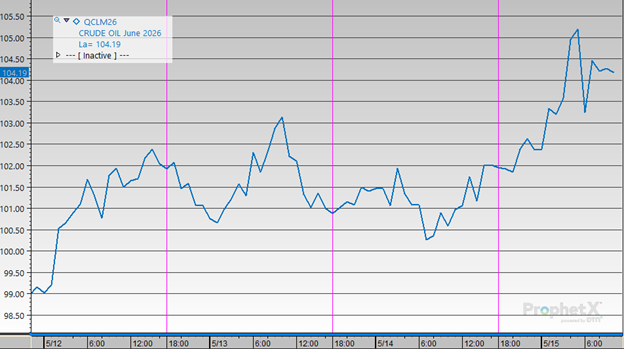

Crude prices moved modestly higher throughout the week, with the strongest gains occurring midweek. Prices opened at $98.19 on Monday and edged up to $98.39 on Tuesday before climbing to $102.16 on Wednesday. The market eased slightly to $101.02 on Thursday and then rose again to $102.06 on Friday. Crude prices increased by $3.87 per barrel, representing an overall 3.9% gain during the week.

Diesel prices moved higher through midweek before giving back those gains toward the end of the period. Prices opened at $3.9483 on Monday, edged up to $3.9815 on Tuesday, and then climbed to $4.1176 on Wednesday. Prices then reversed lower to $3.9700 on Thursday and declined further to $3.9383 on Friday. Overall, diesel prices ended the week relatively flat, closing just $0.0100 per gallon below Monday’s opening level.

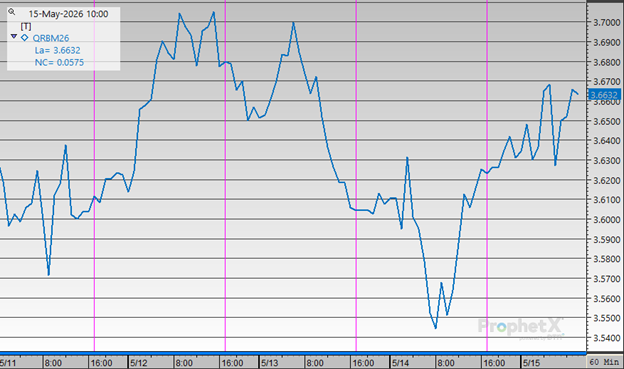

Gasoline prices opened on Monday at $3.5751, increased to $3.5926 on Tuesday, then climbed to $3.6996 on Wednesday. Gasoline prices pulled back to $3.6062 on Thursday before rising slightly to $3.6312 on Friday. Overall, gasoline prices ended the week $0.0561 per gallon above Monday’s opening level, representing an approximate 1.6% increase.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")