2025 Year in Review

FUELSNews will pause for the New Year holiday and resume on Monday, January 5. We wish you a safe and restful start to 2026 and look forward to bringing you our regular market updates after the break.

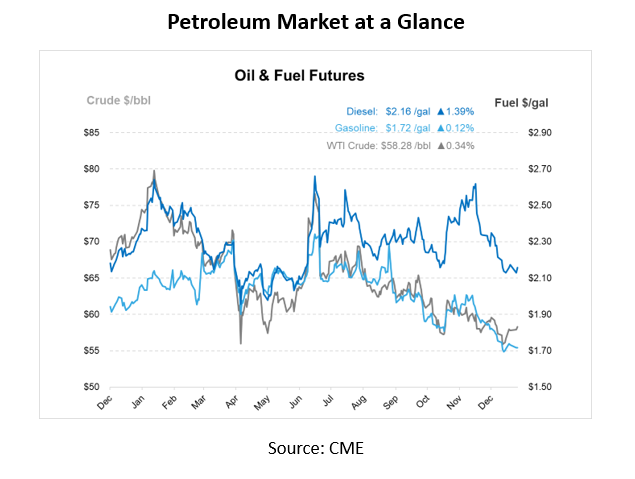

Petroleum markets in 2025 were defined by geopolitical uncertainty, bearish sentiment, and a constant tug-of-war between headline-driven volatility and the gravitational pull of supply fundamentals. Prices moved sharply at times, but by year’s end, crude, diesel, and gasoline had all traveled a long road. From January to December 2025, WTI crude prices fell by roughly $17 per barrel, or about 24%, as early-year supply tightness gave way to record U.S. output, OPEC+ production increases, and mounting expectations of a global oil surplus heading into 2026.

The year opened with bullish sentiment. January crude prices jumped to their highest levels in more than two months as winter weather, tightening inventories, and supply-side anxiety pushed WTI into the low-to-mid $70s and briefly toward $80 per barrel. U.S. crude stocks sat below seasonal norms, refinery utilization remained strong, and distillate inventories tightened as cold snaps boosted heating demand across large portions of the country. Diesel, in particular, carried a firm bid early in the year as heating oil demand overlapped with transportation needs, reinforcing its role as the most sensitive part of the barrel. Infrastructure and policy headlines added fuel to the rally, from the Colonial Pipeline disruption in January to renewed attention on U.S. offshore drilling restrictions and Alaskan land protections.

That early bullish momentum, however, proved difficult to sustain. By February and March, markets were already wrestling with competing forces. Sanctions on Russian oil and heightened enforcement rhetoric kept supply risk in play, but rising refinery runs and product inventory builds introduced a more cautious tone. Tariff headlines began to weigh more heavily, not because energy products were always targeted, but because markets increasingly priced the downstream impact on economic growth and fuel demand. Diesel supply tightened further in late March, with days-of-supply metrics falling to levels that would typically support a seasonal rally, yet prices failed to respond in textbook fashion as macro uncertainty kept buyers on the sidelines.

The real reset arrived in early April. Oil prices fell sharply as tariff escalation fears collided with OPEC+’s decision to accelerate production increases. The combination proved decisive. Crude slid to its lowest levels in more than two years, and both diesel and gasoline followed, marking the market’s clearest pivot away from shortage anxiety and toward surplus concern. Even as sanctions on Iran and Russia periodically reintroduced risk premiums, the underlying message had shifted.

By late spring, that dynamic became increasingly visible at the consumer level. Gasoline prices fell to four-year lows heading into Memorial Day, even as travel demand increased to its highest level in two decades. Refining constraints persisted in the background, but global supply growth expectations and OPEC+ signaling kept crude prices under pressure. Diesel remained the outlier, with inventories falling to historically tight levels in May and backwardation widening in prompt spreads, yet even that strength existed alongside a broader narrative of slowing demand growth.

Summer delivered the most dramatic price movement of the year, and the clearest lesson in how quickly risk can be priced out. In mid-June, crude spiked on fears that conflict between Iran and Israel could disrupt flows through the Strait of Hormuz. When a ceasefire materialized and no major supply outages occurred, the market unwound that premium almost overnight. Crude posted its steepest weekly decline since 2023, falling more than $12 per barrel in a single week, while diesel and gasoline followed with double-digit percentage decreases. It was a stark reminder that geopolitical risk still moves markets, but only as long as barrels are actually threatened.

The second half of the year oscillated between policy-driven volatility and fundamental restraint. U.S. crude production climbed to record levels, topping 13.5 Mbpd, while trade flows shifted as tariffs and sanctions reshaped buyer behavior in China, India, and Europe. Sanctions on Russian energy infrastructure sparked sharp rallies in October, briefly flipping market structure back into backwardation, but those moves faded as inventories rebuilt and supply resilience reasserted itself. Regional dynamics continued to matter, particularly in California, where refinery closures drove sharp retail gasoline price spikes even as national benchmarks softened.

By December, crude prices had slipped back into the mid-to-high $50s, diesel and gasoline followed suit, and the dominant narrative was firmly in place. Strong refinery output, rising non-OPEC supply, and expectations of an oil surplus in 2026 kept rallies short-lived. Even geopolitical headlines struggled to move markets for more than a session or two. The year ended not with a crash, but with a steady drumbeat of caution and a market increasingly comfortable with abundance.

As 2025 comes to a close, the takeaway is not that volatility is gone, rather that the burden of proof has shifted. In 2026, supply is assumed. Demand growth must be earned, and rallies must justify themselves against a backdrop of full tanks and flexible production.

This article is part of Daily Market News & Insights

Tagged: backwardation in oil markets, California refinery closures, diesel price trends, diesel supply shortage, fuel demand forecast, gasoline market outlook, global oil surplus 2026, global refining constraints, oil market 2025, oil market outlook 2026, oil price volatility, Oil Tariffs, OPEC+ production impact, refinery utilization rates

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.