Fuel Prices Ease Heading into Winter. Is Now the Time to Lock in Fuel Costs?

U.S. fuel markets are entering December with a rare stretch of lower prices, as both gasoline and diesel continue to fall. Crude benchmarks remain under pressure, and seasonal demand softness is providing some temporary cost relief to fleets. But beneath the recent declines lie important geopolitical and supply-side developments that could influence price trajectories heading into 2026.

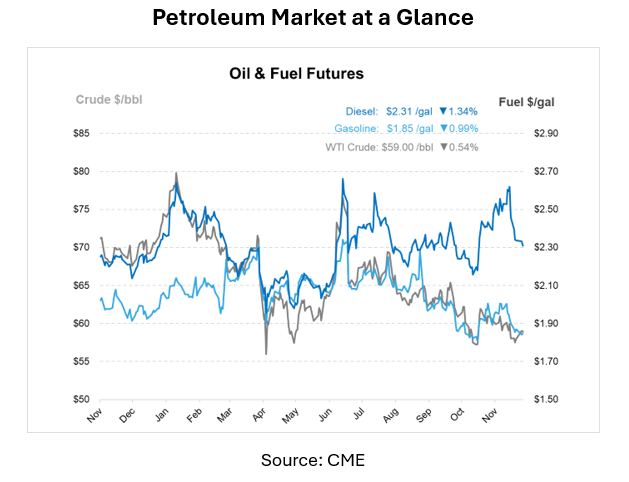

The national average gasoline price fell below $3 per gallon over the weekend, marking the lowest level since 2021, with the median U.S. price now at $2.83/gal. Gasoline is nearly 7 cents cheaper than a month ago and more than 5 cents below year-ago levels, with some retail stations even posting pump prices under $2. Diesel has followed a similar path, sliding to a national average of $3.72/gal, down more than 5 cents over the past week.

These declines provide welcome relief after months of elevated diesel spreads and unsteady wholesale markets. The pullback reflects weaker global crude prices, healthy refinery production, and modest U.S. demand as winter approaches. EIA forecasts suggest that gasoline and diesel prices will continue to decline into 2026, driven largely by lower crude oil benchmarks.

If locking in a fixed fuel price is something you have been considering, now may be the time to make the commitment before volatility returns. Knowing fuel costs in advance allows companies to plan their financial resources more effectively. With Mansfield Fuel Price Risk Management services, you can plan for the unexpected and mitigate the impact of these events on your bottom line.

In geopolitical news, OPEC+ reaffirmed its decision to maintain production levels unchanged through Q1 2026. The group has restored nearly 3 Mbpd since April but is maintaining more than 3.2 Mbpd in cuts. For U.S. markets, this helps stabilize inventory levels, thereby preventing crude benchmarks from rising too sharply.

More importantly, OPEC+ approved a new mechanism to reassess member production capacity, a process that will run through 2026 and determine the baselines used for 2027 quotas. While this has limited immediate price impact, it introduces future uncertainty, as debates over quota fairness have historically caused friction within the group.

Global tensions, including Ukrainian drone strikes on Russian infrastructure and U.S.-Venezuela strains, have injected some geopolitical risk into markets, but not enough to offset structural oversupply. Peace discussions between the U.S., Russia, and Ukraine are ongoing, and while a long-term resolution remains uncertain, even the possibility of increased Russian exports in the future is adding more bearish sentiment to the market.

This article is part of Daily Market News & Insights

Tagged: crude inventory levels, December fuel market trends, fixed fuel pricing, fleet fuel costs, fuel cost planning, fuel hedging, fuel price outlook 2026, fuel price relief, fuel price risk, gasoline prices December, Global oil markets, lower fuel prices 2025, Mansfield Fuel Price Risk Management, price volatility fuel markets, Q1 2026 oil outlook, Russian oil exports, U.S. Venezuela oil tensions, wholesale fuel market

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")