Freight Activity Hits Five-Year Low as US Oil Output Hits Record High: What It Means for Fuel Demand

Fuel demand patterns are shifting as the U.S. freight sector continues to face challenges in light of tariff uncertainty, marking another down month in October, as the Cass Freight Index fell sharply. Shipment volumes dropped 2.1% seasonally adjusted from September and were down 7.8% year-over-year, hitting the lowest level since June 2020. This downturn follows two years of persistent weakness, with Cass noting it has been 40 months since the first year-over-year decline in shipments during this cycle. After strong gains in 2021, the index has posted consecutive annual declines of 5.5% in 2023 and 4.1% in 2024, and is trending toward another drop in 2025.

The report highlights that fleets are under financial pressure, with margins at generational lows and equipment investments curtailed. Highway tractor capacity is contracting as closures accelerate in the for-hire market and private fleet expansion reverses. While freight rates ticked up slightly, Cass’s Linehaul Index rose 1.1% month-over-month in October and 3% year-over-year, but these gains may be temporary. Spot market trends have softened in early November as pre-tariff shipping activity has begun to fade.

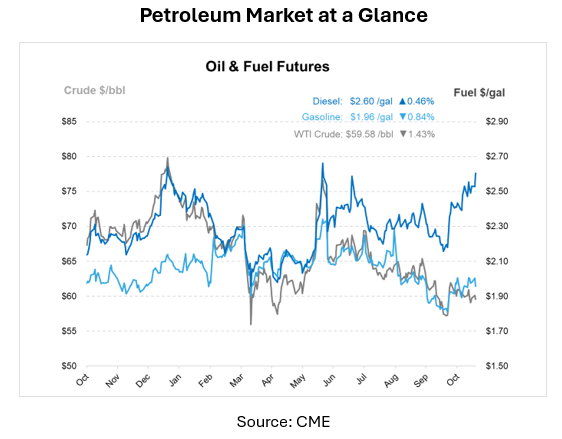

Freight activity is a critical driver of U.S. diesel consumption, and the sustained weakness in shipments signals potential softness in demand. Trucking accounts for more than 75% of shipments tracked by Cass, meaning fewer goods moving across the country translates directly to reduced diesel burn. While diesel margins have recently increased by $7/bbl this month due to tight supply and strong European export demand, the underlying fundamentals suggest caution.

In contrast to freight, U.S. oil and gas production remains robust. The Energy Information Administration (EIA) reports that crude output reached a record 13.86 Mbpd in early November. This growth comes even as the rig count has fallen from its 2022 peak, showing how operational efficiencies, such as longer lateral drilling, advanced hydraulic fracturing, and automation, are sustaining output. Regions like the Permian Basin and Appalachia exemplify this trend, posting double-digit production gains despite a decline in the number of rigs.

The combination of record oil output and a freight recession will determine the path ahead for U.S. fuel demand. Gasoline affordability may improve as crude prices soften, but diesel consumption faces structural headwinds from slowing freight and manufacturing activity.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.