Week in Review – Oil Prices Dip Ahead of OPEC+ Meeting

Crude oil prices fell slightly this morning, with prompt WTI trading down more than 40 cents per barrel. The upcoming OPEC+ meeting this weekend and the release of the U.S. nonfarm payrolls report are expected to influence short-term supply decisions and provide insight into broader economic conditions. Meanwhile, refined product inventories continue to tighten, biofuel imports have dropped significantly, and refinery disruptions abroad are adding complexity to the global supply landscape.

This week, geopolitical headlines have taken center stage. President Trump urged European leaders to stop purchasing Russian crude and called on Europe to place economic pressure on China, citing Beijing’s support of Russia’s wartime economy. He also reaffirmed his commitment to a Russia-Ukraine peace agreement and hinted at the possibility of direct talks between the two nations.

In the meantime, Ukraine escalated the conflict with reported drone strikes on Russia’s Ryazan oil refinery and a fuel depot under Russian control. These attacks raise concerns about supply risks from Russian infrastructure as the winter demand season approaches.

All eyes are now at the OPEC+ meeting scheduled for this weekend. Markets are looking for any shift in production strategy, particularly whether the group will maintain output cuts or begin to ease restrictions in response to current inventory levels and demand signals.

On the supply side, the U.S. Energy Information Administration reported a mixed picture this week. Crude oil inventories rose by 2.4 million barrels, surprising analysts who had expected a draw of 2.0 million barrels. Stocks at Cushing, Oklahoma, one of the country’s largest storage hubs, rose by 1.6 million barrels.

In contrast, gasoline inventories fell sharply by 3.8 million barrels, marking the lowest level since November 2024. The decline has pushed prompt gasoline cracks to $21.07 per barrel, their highest since August 20. Distillate inventories rose by 1.7 million barrels but still sit 13% below the five-year average for this time of year.

Despite the crude build, overall U.S. oil and product inventories remain tight. Crude stocks are 4% below average, gasoline is 2% below, and distillate remains the most undersupplied category. These figures reflect a domestic fuel market that is still trying to balance recovering demand with limited production capacity.

Adding to product tightness, the restart of the 204,000 bpd gasoline unit at Nigeria’s Dangote Refinery has been delayed to September 20. The plant was expected to provide some relief to gasoline markets, but the delay could keep pressure on regional and global supplies in the short term.

In the biofuels sector, U.S. imports of biodiesel and renewable diesel have decreased. According to the EIA, biodiesel imports averaged just 2,000 bpd in the first half of 2025 – down sharply from 35,000 bpd a year earlier. Renewable diesel imports dropped to 5,000 bpd from 33,000 bpd over the same period. The agency attributes the reduction to the expiration of tax credits for imported biofuels and lower domestic demand. These are the lowest import levels recorded since 2012 and suggest that renewable fuel supply could remain tight throughout the rest of the year.

The U.S. economic backdrop is also contributing to market uncertainty. Goldman Sachs Research forecasts a 60,000-job gain in today’s nonfarm payrolls report, below the consensus estimate of 75,000 but above the recent three-month average of 35,000. Government payrolls are expected to fall by 20,000, driven entirely by reductions at the federal level. Historically, August payroll reports tend to be revised upward in subsequent months, so today’s figure may not reflect the final picture.

Elsewhere, Q2 non-farm productivity was revised upward to an annualized rate of 3.3%, signaling improved efficiency in the private sector. However, trade data showed a widening deficit in July, driven largely by gold imports and increased shipments from China. Initial jobless claims also came slightly above expectations, particularly in Connecticut and Tennessee, although continuing claims fell.

As a result of these data points, Goldman Sachs revised its Q3 GDP growth forecast slightly downward to 1.6% annually, while keeping domestic final sales growth unchanged at 0.7%.

This week’s developments point to a market pulled in multiple directions. On one hand, product supply remains tight. especially for gasoline and distillate, amid declining inventories, delayed refinery restarts, and slumping biofuel imports. On the other, economic indicators suggest weaker job growth and softer GDP expansion, which could curb demand growth.

Geopolitical developments and the outcome of the OPEC+ meeting this weekend will likely shape next week’s price direction. Until then, markets remain in a holding pattern, balancing bullish supply-side fundamentals with cautious demand-side expectations.

Prices in Review

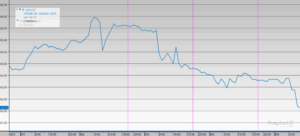

Following the Labor Day Holiday, crude prices decreased throughout the week, with the most significant losses occurring in the second half. Prices edged up slightly on Tuesday, climbing to a weekly high of $64.96. However, by Wednesday, values had dropped to $64.24, and Thursday saw the sharpest single-day decrease, falling by $1.05 to $63.19. The downward trend continued into Friday, when prices reached the weekly low of $62.24. Overall, crude fell by $2.58, or 3.98%, for the week.

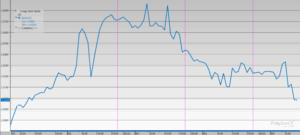

Diesel prices rose early in the week before reversing course. On Tuesday, diesel opened at $2.3354 and climbed steadily to a weekly high of $2.3656 on Wednesday, marking the largest single-day gain. However, prices fell on Thursday to $2.3099 and continued to slip on Friday, opening at $2.2967. Overall, diesel ended the week down -$0.0014, or -0.06%.

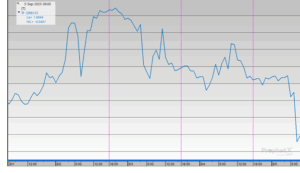

Gasoline prices followed a mild upward trend early in the week, rising to a peak of $2.0196 on Wednesday. However, prices began to ease on Thursday and fell more sharply on Friday, opening at $1.9678. This marked a loss of $0.0255, or -1.28%, for the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")