Weekend Israel-Iran Attacks Push Oil Prices Higher

The Middle East conflict continues to keep energy markets on alert, with renewed attacks between Israel and Iran adding pressure to an already uncertain supply picture. Over the weekend, Israel struck targets in western and central Iran, while Iranian state media reported multiple explosions in Tehran. Iran responded with missile attacks toward Israel, which the Israel Defense Forces said were identified and intercepted, with no casualties reported. President Trump urged both sides to “stop shooting immediately” and called for more time for diplomacy.

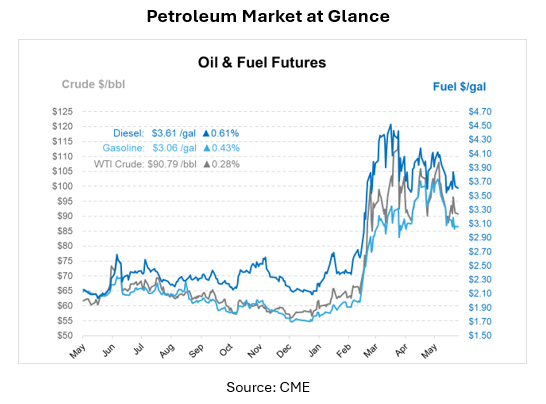

Oil prices moved higher as the renewed attacks raised concerns about whether the conflict could spread further or disrupt more energy infrastructure. WTI futures were trading up by more than $1 per barrel this morning after closing about $3 per barrel higher week over week. Prices had risen as much as 5% following the latest wave of attacks before giving back part of those gains after Iran said its first wave of strikes had ended.

Shipping remains one of the biggest concerns. With that route restricted, Gulf producers and energy buyers have fewer options, and any additional disruption can quickly affect global supply expectations. Iraq’s foreign minister warned that the country may be unable to pay public salaries next month if the strait remains closed, noting that Iraqi crude exports are currently limited to the Kurdistan pipeline at about 200,000 barrels per day.

The Red Sea is also drawing attention. Yemen’s Iran-aligned Houthis announced a ban on Israeli maritime navigation in the Red Sea and said enemy movements would be treated as legitimate military targets. While the announcement does not apply to all commercial shipping, it adds uncertainty to a route that has become more important as Hormuz remains restricted. The Red Sea and Suez Canal are key shipping corridors, and any threat there can force vessels to consider longer routes around Africa, adding time, fuel costs, and insurance costs to deliveries.

That risk matters even more because Red Sea traffic has not fully recovered from previous Houthi attacks. Major shipping companies rerouted vessels around Africa during earlier disruptions, and average monthly sailings through the southern Red Sea and Bab al-Mandab Strait remain below pre-2023 levels. If the threat expands beyond Israeli-linked vessels or if shippers decide the risk is too high, the impact could reach broader commercial and energy flows.

Supply signals remain mixed. OPEC+ agreed to increase crude output quotas for July by 188,000 barrels per day. Saudi Arabia and Russia received the largest increases, at 62,000 barrels per day each, followed by Iraq at 26,000 barrels per day and Kuwait at 16,000 barrels per day. Saudi Arabia also lowered crude prices for all grades by about $10 per barrel for customers in Europe and the Mediterranean following the OPEC+ decision. These moves could help ease some price pressure, but the added supply may not fully offset the risk of disruptions in key shipping lanes.

Demand is another important part of the story. Goldman Sachs Investment Research estimated that global oil demand destruction reached 4 million to 5 million barrels per day in April. According to the estimate, the Hormuz shock appears to have reduced global demand by about 4% to 5% compared with a no-war scenario. That means the market is not only watching possible supply losses, but also signs that high prices, disrupted trade flows, and weaker activity may be weighing on consumption.

Broader economic conditions are also shaping the outlook. U.S. nonfarm payrolls rose by 172,000 in May, well above expectations, while the unemployment rate held near 4.3%. The stronger labor market has reduced expectations for near-term Federal Reserve rate cuts. Goldman Sachs Investment Research now expects the final rate cuts in its forecast to move to June and December of 2027, citing stronger employment data and less urgency for the Fed to lower rates.

For fuel buyers, this matters because interest rates, inflation, and economic activity all influence demand. A stronger labor market can support fuel consumption, but higher-for-longer interest rates can pressure future business investment and consumer activity. At the same time, energy-related inflation from the war remains a risk, even though Goldman Sachs noted it has not yet seen signs that the inflation shock is becoming self-sustaining.

For now, volatility is likely to continue. A sustained pause in attacks, added OPEC+ supply, and weaker demand could help limit further price increases. But renewed fighting, additional shipping disruptions, attacks on energy infrastructure, or setbacks in diplomacy could quickly push prices higher again.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")