Week in Review – Oil Prices Hold Weekly Gains as Supply Risks Remain

Oil prices were relatively steady on Friday morning, but the market is still on track for a strong weekly gain. WTI futures were trading mostly flat early in the day, while still sitting about $6 per barrel higher compared to last week. That gain reflects the tug-of-war currently shaping the oil market: ongoing Middle East supply risks are supporting prices, while ceasefire headlines, weaker demand signals, and expectations of additional OPEC+ supply keep prices from rising further.

A major driver this week has been the ongoing uncertainty over the Middle East conflict. Crude prices sold off by about $3 per barrel on Thursday after reports suggested Israel and Hezbollah had reached a conditional ceasefire agreement, and President Trump said talks with Iran were in the “final” stages. Those headlines briefly gave the market hope that geopolitical risk could ease.

But that optimism did not last long. Later reports said Hezbollah rejected the conditions of the ceasefire announced by the U.S. State Department. Hezbollah leader Naim Qassem also rejected a U.S.-brokered agreement between Israel and the Lebanese government to halt the fighting. Iran has made a ceasefire in Lebanon a condition for any peace deal with Washington, which means the situation remains tied to broader U.S.-Iran negotiations.

Another supply concern came from Oman, where an explosion near the Mina al Fahal oil export terminal initially raised concerns about loading disruptions. Oman later said operations were proceeding normally and that the port was unaffected. The update helped stabilize prices on Friday, but the headline was another reminder of how sensitive the market has become to any potential disruption in the region. Oman exports about 800,000 to 900,000 barrels per day of crude from that terminal.

At the same time, supply concerns are not limited to the Middle East. U.S. crude exports have surged as global refiners look for replacement barrels. U.S. crude exports reached a record 5.6 million barrels per day in May as Asian and European refiners turned to American oil to help offset disrupted Middle East supply.

That export strength is drawing down U.S. inventories. Cushing, Oklahoma, the delivery point for WTI crude futures, has seen inventories fall quickly. Stocks at Cushing dropped to 22.4 million barrels as of May 29, down about 4 million barrels from late February.

The concern is that Cushing could move closer to operational minimum levels. When inventories fall too low, it can create challenges moving crude between tanks, blending crude properly, and maintaining smooth outbound flows. That is especially important for Midwest refiners that depend heavily on Cushing because they do not have the same access to seaborne imports as coastal refiners.

OPEC+ is also expected to add more supply. The group is set to increase production quotas at least three more times this year as it continues restoring supply that was previously cut in 2023. OPEC has also kept its oil demand growth forecast unchanged at 1.2 million barrels per day for this year, signaling that the group still expects demand to remain resilient despite the conflict and ongoing market volatility.

Economic data is adding another layer of caution. The May payrolls preview pointed to slower job growth, with estimates showing nonfarm payrolls rising by 60,000, below the consensus estimate of 85,000. The unemployment rate was expected to remain unchanged at 4.3%. A softer labor market can raise questions about future fuel demand, especially if broader economic activity begins to slow.

Prices in Review

Crude prices moved higher through most of the week before pulling back on Friday. Prices opened at $88.50 on Monday and climbed to $92.45 on Tuesday, continuing higher to $93.45 on Wednesday. The rally extended to $95.75 on Thursday, before prices retreated to $92.82 on Friday. Despite the late-week decline, crude finished above its opening level, gaining $4.32 per barrel, or approximately 4.9%, during the week.

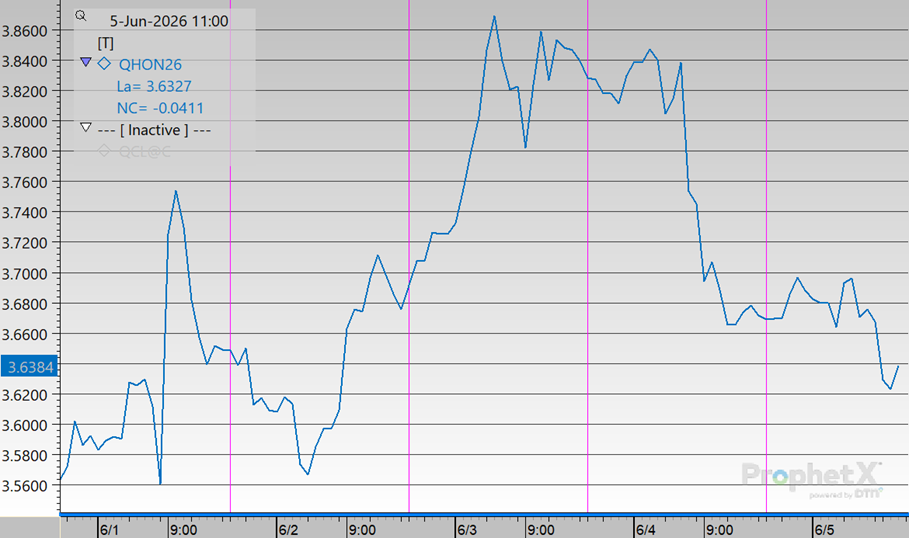

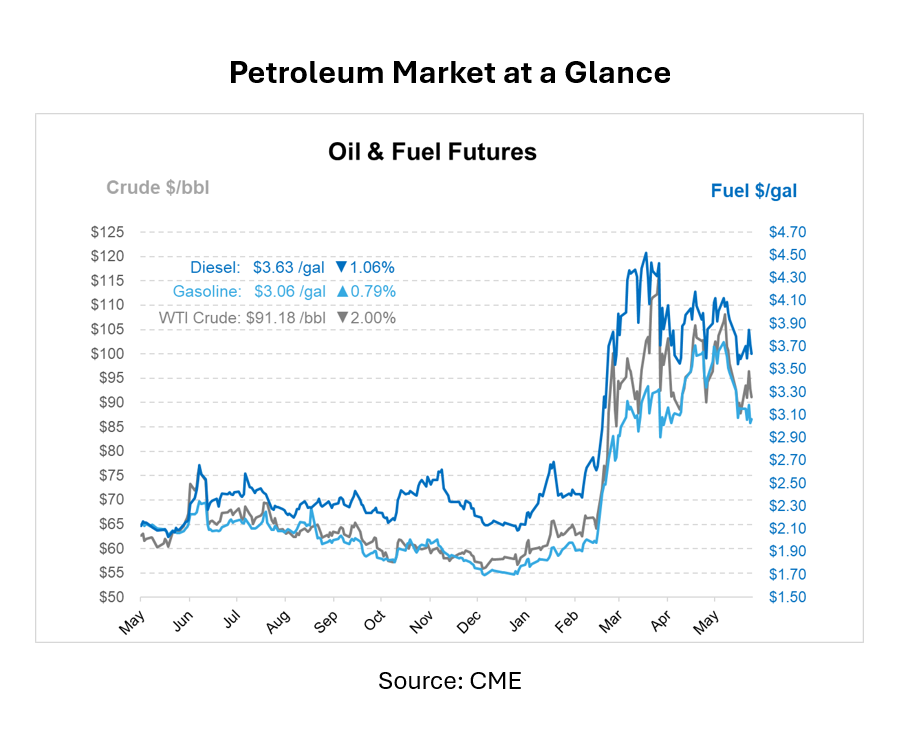

Diesel prices advanced steadily through most of the week before retreating on Friday. Prices opened at $3.5448 on Monday and rose to $3.6494 on Tuesday, followed by additional gains to $3.6831 on Wednesday. Prices continued higher to $3.8287 on Thursday, before pulling back to $3.6730 on Friday. Despite the late-week decline, diesel prices rose $0.1282 per gallon, an approximate 3.6% increase.

Gasoline prices rose steadily through most of the week before reversing on Friday. Prices opened at $3.0547 on Monday and rose to $3.0826 on Tuesday, then advanced to $3.1239 on Wednesday and $3.1415 on Thursday. Prices pulled back to $3.0400 this morning. Overall, prices decreased $0.0147 per gallon, representing an approximate 0.5% decline throughout the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")