EIA Outlook Signals Long-Term Impact From Strait of Hormuz Disruptions

Global oil markets are navigating one of the most unstable periods seen in years as the disruption surrounding the Strait of Hormuz continues to reshape global energy flows. In its latest outlook, the U.S. Energy Information Administration (EIA) warns that the effects of the conflict are expected to last well beyond the immediate supply disruption, even if vessel traffic through the Strait begins recovering within the next week. The agency now believes the impacts on oil production, inventories, shipping patterns, and fuel pricing could continue throughout 2026 and potentially into early 2027.

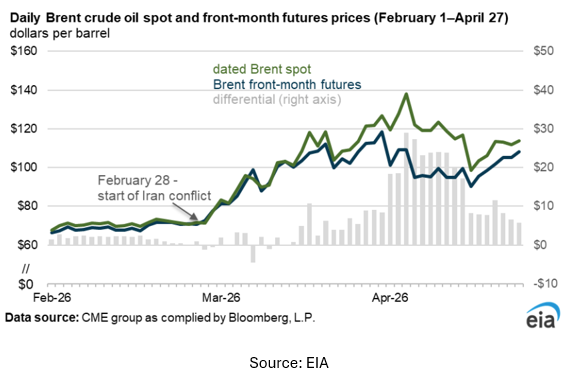

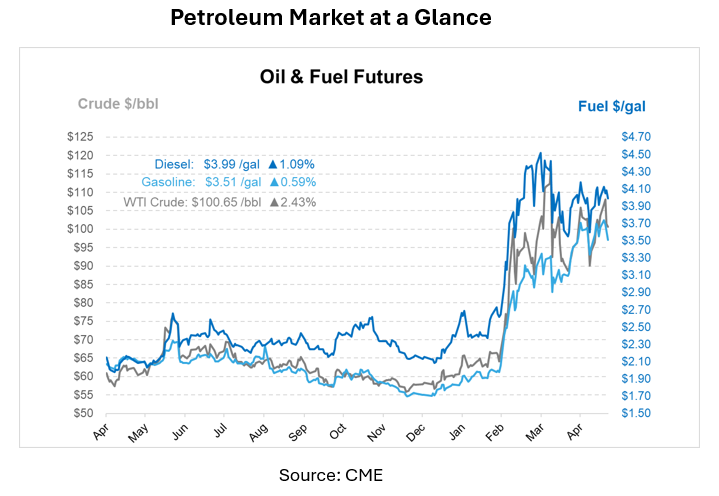

The Strait of Hormuz remains one of the world’s most critical energy chokepoints, normally handling nearly 20% of global oil supply. Since the conflict escalated earlier this year, traffic through the region has slowed dramatically due to both security risks and restrictions affecting Iranian oil exports. The result has been a sharp tightening of available global crude supplies. Brent crude prices averaged $117 per barrel in April alone, roughly $46 per barrel higher than February averages, while daily prices briefly surged to $138 per barrel during some of the market’s most volatile trading sessions.

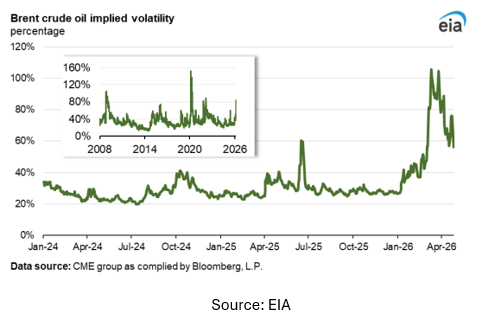

That volatility has become one of the defining characteristics of today’s oil market. According to the EIA, Brent crude implied volatility has averaged 78% since the conflict began, with some sessions climbing above 100%. Before the disruption, implied volatility had generally stayed below 30% for most of 2024. Those large swings highlight how uncertain the market remains around the duration of supply disruptions, the timing of shipping recoveries, and the ability of producers and refiners to replace missing barrels. Physical crude prices also sharply outpaced futures markets earlier this spring, with spot crude trading nearly $30 per barrel above front-month futures contracts at one point as buyers scrambled for immediate supply.

The disruption is not limited to shipping traffic alone. The EIA estimates that production shut-ins across Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain averaged roughly 10.5 million barrels per day in April and could peak near 10.8 million barrels per day in May as storage capacity fills and producers are forced to reduce output further. Iran is also expected to face further production cuts as export restrictions and blockades continue limiting the country’s ability to move crude to market.

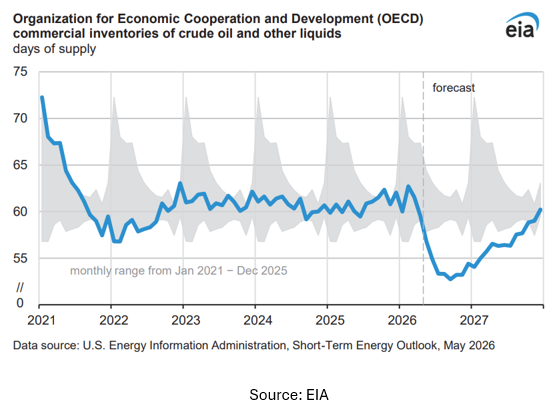

Those supply losses are already having a major impact on global inventories. Earlier this year, markets believed large global stockpiles and floating storage would help absorb temporary disruptions. However, as the conflict dragged on longer than initially expected, inventories have continued falling at a much faster pace. The EIA now expects global oil inventories to decline by an average of 8.5 million barrels per day during the second quarter of 2026. That tightening is expected to keep upward pressure on both crude and refined fuel prices throughout the year, even after flows through the Strait begin gradually recovering.

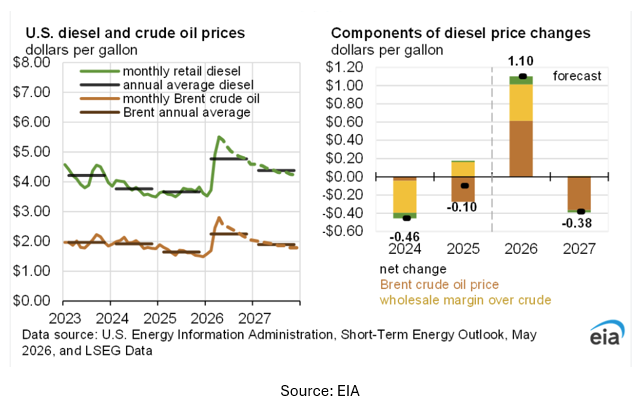

The ripple effects are extending directly into fuel markets. The EIA significantly increased its gasoline price forecast and now expects retail gasoline to average $3.88 per gallon this year and $3.62 next year. Diesel markets also remain under pressure as refining systems and global trade flows continue adjusting to disrupted crude supplies. The agency expects diesel prices to average $4.76 per gallon in 2026. Elevated diesel prices remain especially important for trucking fleets, industrial users, agriculture, and fuel-intensive industries that depend heavily on distillate fuel.

At the same time, the report notes that high prices are beginning to slow global demand growth. Governments in several regions are implementing fuel-saving measures, while some countries are reducing refined product exports and managing shortages. The EIA now expects global oil demand growth to increase by only 0.2 million barrels per day in 2026, sharply lower than earlier forecasts issued before the disruption intensified. Much of that slowdown is expected to occur in Asia, where economies remain highly dependent on Middle Eastern crude supplies.

Higher prices are also encouraging additional production growth outside the region, particularly in the United States. The EIA now forecasts U.S. crude production to reach record levels over the next two years, averaging 13.65 million barrels per day in 2026 before climbing above 14 million barrels per day in 2027. Still, the agency notes that shale growth and other supply responses take time, meaning new production may not arrive quickly enough to offset near-term disruptions.

Even if tensions begin easing soon, the report suggests markets are likely to continue carrying a significant geopolitical risk premium for the foreseeable future. The EIA estimates that if reopening of the Strait were delayed by another month, crude prices could climb more than $20 per barrel above current forecasts in the near term, with elevated prices continuing into next year. For fuel buyers, fleets, and energy consumers, the latest outlook reinforces that the current market is being driven not only by supply and demand fundamentals, but also by uncertainty, logistics disruptions, and ongoing geopolitical risk.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.