Week in Review – Oil Holds Weekly Gains as Hormuz Disruptions Keep Supply Tight

Oil prices are holding near recent highs as the market balances tight supply conditions with rapidly shifting geopolitical headlines. Even with some pullback on news of potential Iran-U.S. talks, prompt WTI futures are still on track to finish the week up by about $11 per barrel. The underlying story hasn’t changed: restricted flows through the Strait of Hormuz and the ongoing U.S. naval blockade of Iranian exports continue to squeeze global supply, keeping upward pressure on crude despite day-to-day volatility.

Physical supply conditions are making most of the heavy lifting behind higher prices. The blockade has effectively choked off Iranian exports, with trackable shipments down more than 80% since March. Only about 4 million barrels of crude were able to leave the Gulf of Oman in mid-April, while dozens of tankers holding an estimated 69 million barrels are now sitting in floating storage, with nowhere to go. At the same time, the Strait of Hormuz remains largely closed, restricting flows not only from Iran but also from major producers such as Saudi Arabia, the UAE, Kuwait, and Iraq. While a handful of vessels, including a Pakistani tanker this week, have managed to transit the Strait, traffic remains extremely limited and unpredictable.

The supply shock is now spreading well beyond crude. Refined products, especially jet fuel, are showing the clearest signs of strain. Europe, which relies heavily on imports from the Middle East and Asia, is facing the risk of critically low jet fuel inventories as early as late May. Some projections suggest reserves could fall below a 23-day supply threshold, raising the possibility of rationing, reduced flight schedules, and higher ticket prices. Unlike diesel or gasoline, jet fuel faces structural constraints, including limited storage and refining flexibility, making it more vulnerable to sudden disruptions. As Europe scrambles to pull in supplies from the U.S. and West Africa, global competition for barrels is intensifying, pushing prices higher across the board.

Meanwhile, geopolitical risks continue to build. Ukrainian drone strikes on Russian energy infrastructure this week knocked out a key processing unit at a 260,000 bpd refinery, adding another layer of disruption to an already tight market. In the Middle East, tensions remain elevated despite a ceasefire technically being in place since early April. Iranian officials have warned of “long and painful strikes” if the U.S. resumes attacks, while U.S. leadership is actively reviewing options for further military action. At the same time, trust between regional players remains low, with UAE officials openly questioning whether Iran can be relied upon to ensure safe passage through Hormuz under any unilateral arrangement.

Governments are trying to respond, but their tools are limited. The U.S. continues to lean on the Strategic Petroleum Reserve (SPR), releasing 17.5 million barrels last week and offering to loan up to 92.5 million more barrels to companies to stabilize markets. Even so, total SPR inventories now sit around 398 million barrels, roughly equivalent to just a few days of global demand. While these releases help at the margin, they have not been enough to offset the scale of disruption caused by the blockade. The International Energy Agency has already described the situation as the largest oil supply disruption in history, underscoring the magnitude of the challenge.

Looking ahead, attention is turning to upcoming policy and supply decisions. OPEC+ is set to meet in June to discuss continued production increases, though the UAE’s recent decision to exit the group raises questions about cohesion and future strategy. In North America, new infrastructure developments are also in focus, including a newly authorized project to transport up to 550,000 bpd of Canadian crude to Wyoming, which could help improve regional supply flows over time.

For now, the oil market remains caught between physical tightness and the constant possibility of a geopolitical breakthrough. Prices may continue climbing due to supply constraints, but sharp pullbacks remain likely whenever there is even a hint of progress toward reopening the Strait of Hormuz. Until that corridor is fully restored, volatility is expected to remain elevated, and the risk of further price spikes is on the table.

Prices in Review

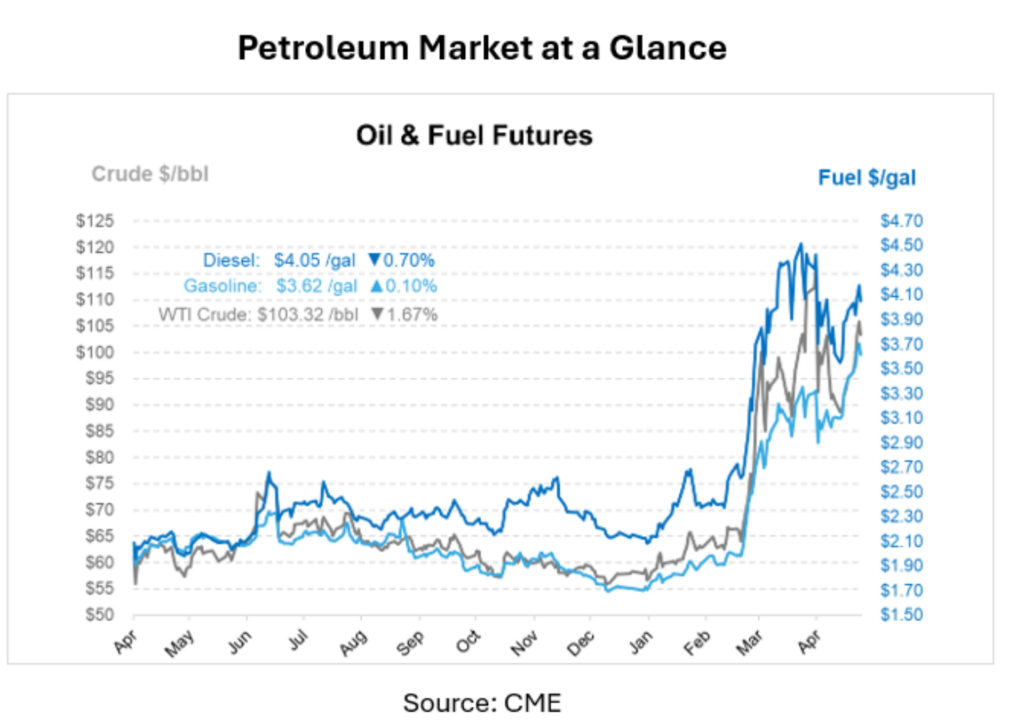

Crude prices climbed sharply through most of the week before pulling back at the end. Prices opened at $95.60 on Monday, rose to $96.67 on Tuesday, and then increased further to $99.71 on Wednesday. The rally accelerated on Thursday, with prices opening at $109.07. By Friday, crude opened at $105.14, up $9.54 per barrel, for an overall 10.0% gain during the week.

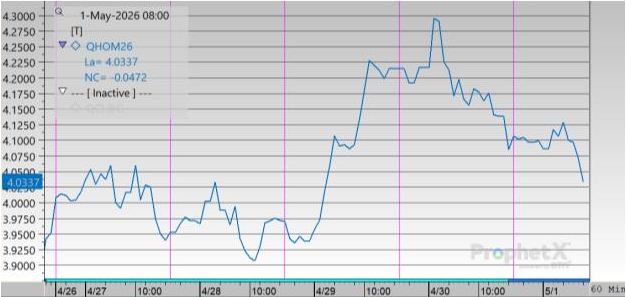

On Monday, diesel prices opened at $3.9812, then dipped to $3.9383 on Tuesday, before edging up to $3.9706 on Wednesday. Price then rose to $4.1916 on Thursday, before pulling back to $4.0940 on Friday. From Monday to Friday, diesel prices rose by $0.1128 per gallon, a 2.8% gain.

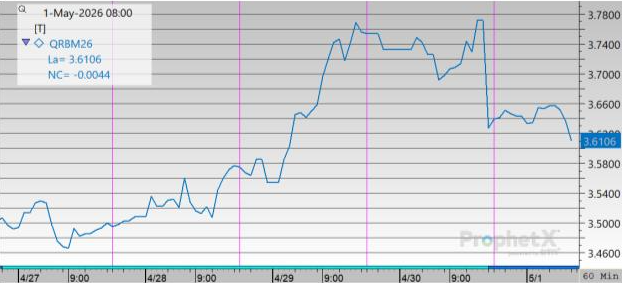

Gasoline prices opened on Monday at $3.4992 and edged slightly lower to $3.4913 on Tuesday. Prices then strengthened to $3.5747 on Wednesday and surged to $3.7535 on Thursday. By Friday, gasoline pulled back to $3.6311 but remained above its start-of-week level. From Monday to Friday, gasoline prices rose by $0.1319 per gallon, representing a 3.8% increase.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")