Week in Review – Prices Pull Back, But the Market Remains Tight

Energy markets are closing the week with a noticeable shift in price direction, but not a meaningful easing in underlying pressure. Crude has pulled back following the announcement of a two-week ceasefire between the U.S. and Iran, with prompt WTI now down more than $13 per barrel week-over-week. Even with that decline, prices are still holding in the upper $90s, reflecting a market that has eased on sentiment but not on fundamentals.

While the ceasefire has eased immediate fears, physical oil flows have not meaningfully recovered. Current estimates show oil exports through the Strait of Hormuz at roughly 1.5 million barrels per day, just about 8% of normal levels. Broader Persian Gulf flows are also reduced, running at less than one-third of typical volumes. Until those barrels return to the market, crude prices are likely to remain supported, even with ongoing diplomatic progress.

At the same time, the situation on the ground continues to add risk back into the market. The ceasefire has not fully held, with continued fighting involving Hezbollah in Lebanon raising questions about how durable the agreement really is. Markets are reacting to this mixed signal, pricing in some level of de-escalation while still carrying a geopolitical risk premium.

Supply disruptions are also becoming more defined and more impactful. Attacks on Saudi energy infrastructure have taken approximately 600,000 barrels per day of production offline, while flows on the East-West Pipeline have been reduced by another 700,000 barrels per day. That pipeline has become a critical alternative export route while the Strait of Hormuz remains restricted, so any disruption there has an outsized impact on global supply availability. In practical terms, fewer barrels are reaching the market, and the system has less flexibility to respond.

There are early signs that producers are preparing for a recovery, but not executing one yet. Middle Eastern suppliers have begun asking buyers to submit crude loading schedules for April and May, signaling that they are positioning for a potential restart of exports. However, vessel traffic remains extremely limited, and restrictions, including requirements for ships to coordinate directly with Iranian authorities, are slowing any meaningful normalization.

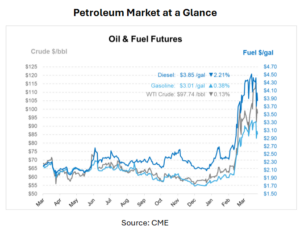

Refined product markets continue to show even tighter conditions than crude. Diesel, in particular, remains under significant pressure globally. The Middle East is a major supplier of diesel and high-yield crude grades, and disruptions there are directly impacting availability. As a result, diesel prices are holding strong and, in many cases, continuing to rise relative to crude. Gasoline is also firm, though less constrained than diesel, as global refining systems adjust to shifting crude flows and product demand.

U.S. refiners are playing a key role in balancing the market. Refinery utilization has climbed to around 92%, with Gulf Coast facilities running above 95%. That high throughput is allowing the U.S. to export record volumes of refined products into undersupplied international markets. While that helps offset global shortages, it also keeps domestic prices elevated, as barrels are pulled toward higher-priced export markets.

Beyond the energy complex, the impact is already flowing through to the broader economy. U.S. consumer prices rose sharply in March, with one of the largest monthly increases in recent years. Energy costs were a key contributor, with gasoline prices moving above $4 per gallon and diesel driving higher transportation and goods costs. These early inflation signals suggest that even a short-term disruption in energy markets can quickly translate into broader economic pressure.

What This Means for Prices

Right now, the market is balancing two competing forces. On one side, there is growing optimism around diplomacy and a potential reopening of the Strait of Hormuz. On the other hand, there is the reality of ongoing supply disruptions, reduced production capacity, and limited physical flows.

Until flows return in a meaningful way, and infrastructure disruptions are resolved, prices are likely to remain supported. Even with short-term pullbacks like the one seen this week, the broader structure of the market continues to point to tight supply conditions.

Prices in Review

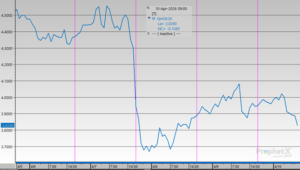

On Monday, crude opened at $112.96 and held relatively steady at $112.62 on Tuesday before declining to $108.74 on Wednesday. Prices then dropped to $96.78 on Thursday, before recovering slightly to $98.23 on Friday. Throughout the week, crude prices decreased by $14.73 per barrel, representing an overall 13.0% decline.

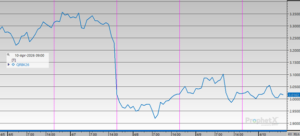

Diesel prices opened at $4.4432 on Monday, slipped to $4.3709 on Tuesday, and then continued downward to $4.2831 on Wednesday. A sharper drop followed on Thursday to $3.8933, the week’s lowest level, before a modest rebound to $3.9524 on Friday. From Monday to Friday, diesel prices fell by $0.4908 per gallon, representing an overall 11.0% decrease.

Gasoline prices trended lower throughout the week. On Monday, prices opened at $3.3060 and edged down to $3.2962 on Tuesday, then fell further to $3.2001 on Wednesday. On Friday, gasoline opened at $3.0139, representing an overall decrease of $0.2921 per gallon, or 8.8%, during the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")