Week in Review – Oil Prices Ease as Negotiations Reduce Near-Term Supply Risk

Oil markets are ending the week under bearish pressure as easing geopolitical fears collided with tightening diesel fundamentals, leaving crude prices lower despite signs of strengthening physical demand in the U.S.

Midweek inventory data from the U.S. Energy Information Administration (EIA) surprised to the bullish side, reporting a 3.5 million barrel draw in crude stocks for the week ended January 30. Cushing, Oklahoma inventories fell by 0.7 million barrels, while distillate stocks posted a sharp 5.6 million barrel draw. Gasoline inventories rose by 0.7 million barrels.

U.S. crude inventories now sit roughly 4% below the five-year average, while distillate inventories are about 2% below seasonal norms. Gasoline remains comparatively well supplied at approximately 4% above average. Recent winter storms Fern and Gianna drove a notable spike in diesel demand, leading to the outsized distillate draw and reinforcing backwardation across diesel futures. Gasoline stocks, by contrast, showed little reaction and illustrate how weather-driven consumption remains concentrated in middle distillates.

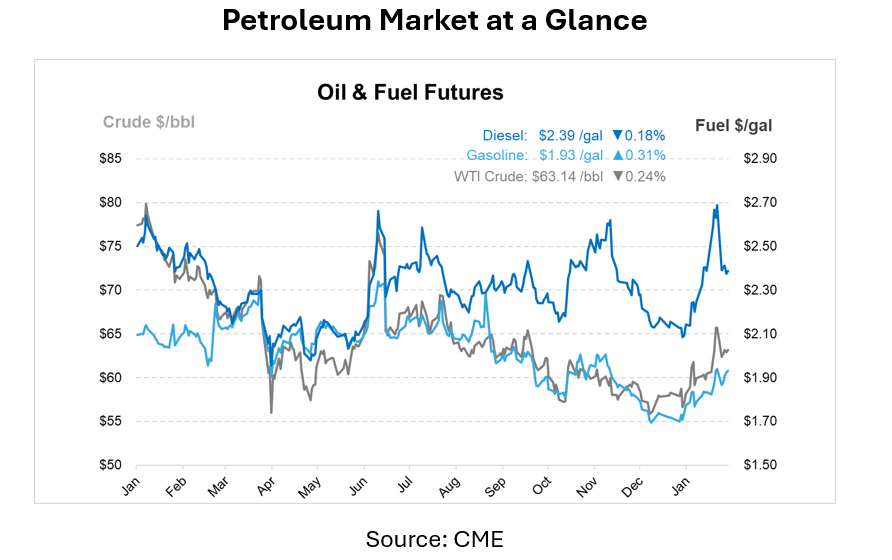

Despite these tightening product balances, crude futures retreated late in the week as markets dialed back risk premiums tied to Middle East tensions. Brent and WTI fell more than 2% Thursday after the U.S. and Iran agreed to hold talks in Oman, easing fears of near-term supply disruptions. Brent hovered near $67.50 per barrel this morning, while WTI traded around $63.18, leaving Brent down roughly 4.6% on the week and WTI lower by about 3.2%.

Investors remain highly sensitive to developments surrounding Iran, given that roughly a fifth of global oil consumption passes through the Strait of Hormuz. While any breakdown in negotiations could quickly reignite price volatility, analysts increasingly point to weak underlying fundamentals. Saudi Arabia announced another cut to its official selling prices to Asia, marking a fourth consecutive month of reductions and further pushing expectations of an oversupplied market.

Market volatility has also driven record trading activity. January saw unprecedented volumes in WTI Midland contracts on Intercontinental Exchange as traders rushed to lock in prices against geopolitical uncertainty and rising Venezuelan exports to the U.S. Gulf Coast. Severe winter weather further complicated supply dynamics, temporarily curbing as much as 2 million barrels per day of U.S. production at peak disruption.

Prices in Review

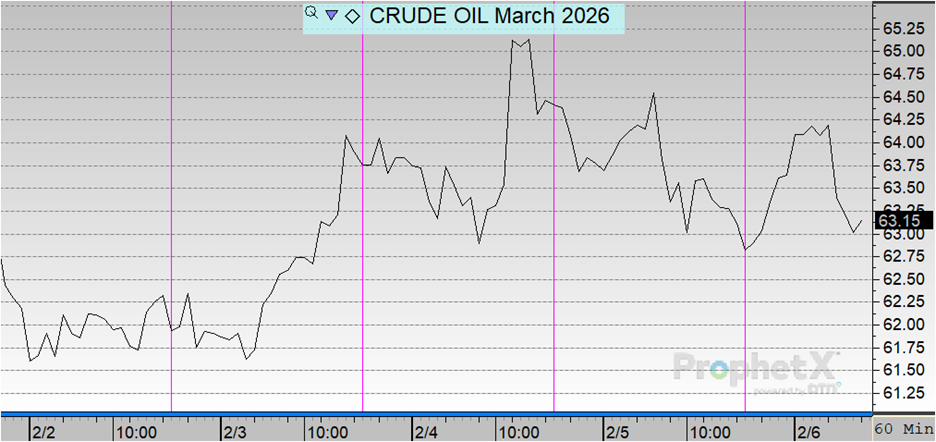

Crude opened the week at $64.72 on Monday before sliding to $62.28 on Tuesday. Prices jumped up midweek, climbing to $63.80 on Wednesday and reaching a weekly high of $64.49 on Thursday. However, those gains failed to hold, with crude settling at $63.10 on Friday. Overall, crude prices declined by $1.62 over the course of the week, representing a 2.50% decrease.

Diesel opened the week at $2.5152 on Monday before falling sharply to $2.3717 on Tuesday. Prices increased midweek, rising to $2.4329 on Wednesday and edging higher to $2.4473 on Thursday. However, those gains failed to hold, with diesel settling at $2.3948 on Friday. Overall, diesel prices declined by $0.1204 over the course of the week, representing a 4.79% decrease.

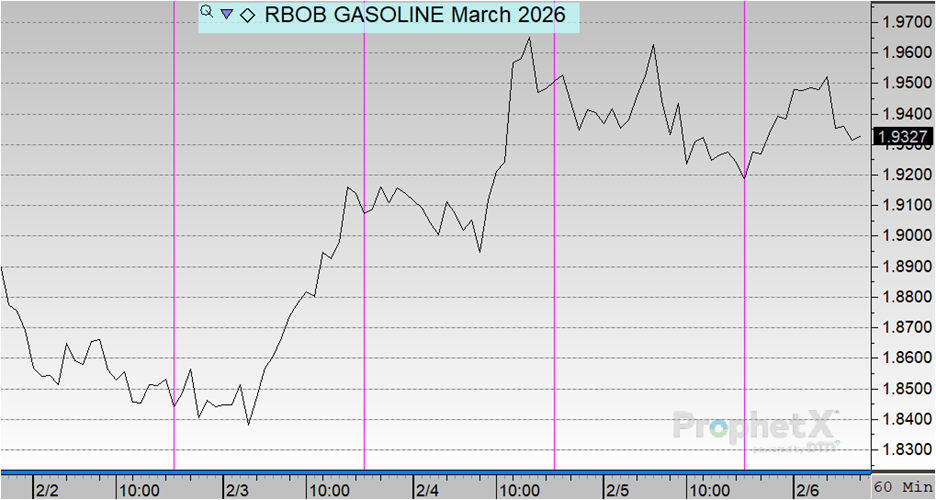

Prices opened the week at $1.9399 on Monday before sliding to $1.8546 on Tuesday. On Wednesday, prices increased to $1.9054, then climbed to a weekly high of $1.9489 on Thursday. However, those gains failed to hold, with prices settling at $1.9250 on Friday. Overall, prices declined by $0.0149 over the course of the week, representing a 0.77% decrease.

This article is part of Daily Market News & Insights

Tagged: Crude oil prices, diesel demand spike, diesel market trends, distillate inventories, fuel supply chain, gasoline inventories, gasoline supply trends, geopolitical risk oil markets, Global oil markets, oil market update, oil supply outlook, petroleum economics, petroleum market analysis, refinery demand trends, U.S. crude stocks, winter storms impact energy

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")