Oil Markets Slide as Geopolitical Risks Collide with Bearish Supply Outlook

FUELSNews will pause for the Christmas holiday and return on Monday, December 29. We wish you and your family a safe, restful, and joyful holiday, and we look forward to publishing our regular market updates after the break.

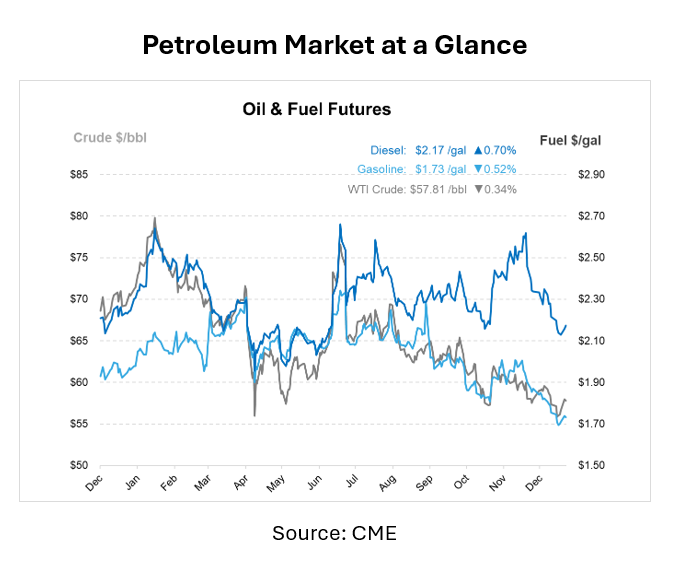

Oil prices are declining this week as markets weigh escalating geopolitical risks against a still-bearish global supply backdrop. After posting their strongest daily gains in weeks on Monday, crude benchmarks are down today, reflecting a market caught between near-term disruption risks and longer-term expectations of ample supply.

Brent crude is holding near the low-$60s per barrel, while WTI remains anchored around $57/bbl. Monday’s uptick was fueled by rising tensions tied to Venezuelan exports and renewed attacks on maritime infrastructure in the Black Sea region. However, follow-through buying has been limited as fundamentals continue to point toward an oversupplied market heading into 2026.

Geopolitical developments remain a key source of headline risk. The U.S. has intensified pressure on Venezuela, with President Donald Trump stating that seized Venezuelan crude could either be sold or retained by the United States. While these actions raise the possibility of tighter Venezuelan exports, actual loadings have remained relatively steady so far, tempering immediate supply concerns.

At the same time, military activity between Russia and Ukraine has intensified around the Black Sea. Ukrainian strikes have damaged Russian vessels, port infrastructure, and piers, while Russia has targeted Ukrainian ports. Ukraine has increasingly focused on disrupting Russia’s “shadow fleet” of tankers used to bypass sanctions, adding risk to Russian crude flows. Still, Russian exports have proven resilient, supported by steady output and refinery disruptions that have pushed more barrels into the export market.

Despite these flashpoints, broader supply fundamentals remain bearish. Expectations remain that the global oil market will be well supplied through the first half of 2026. Barclays projects that while a surplus is likely to persist, it could narrow to roughly 700,000 bpd by late 2026 if Venezuelan and Russian disruptions are prolonged. For now, the balance of risk remains skewed toward oversupply rather than shortage.

One of the most significant structural shifts in the oil market is the growing influence of China. As the world’s largest crude importer, China has effectively replaced OPEC+ as the primary price stabilizer. Throughout 2025, China absorbed excess global supply by increasing crude purchases for storage when prices fell and slowing imports when prices rose, essentially creating an informal price floor and ceiling that kept Brent near $65/bbl.

China’s buying behavior is now one of the biggest unknowns for 2026. Estimates suggest the country still has room to add hundreds of millions of barrels to strategic storage, particularly as new tank capacity comes online. If Beijing continues stockpiling at recent rates, much of the projected global surplus next year could be quietly absorbed into Chinese tanks, limiting downside risk for prices.

In Asia, floating storage surged to a three-year high in recent months as sanctioned oil from Iran, Russia, and Venezuela searched for buyers through soft demand. That buildup now appears to be peaking, with Chinese refiners increasing purchases thanks to wider discounts and new import quotas.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")