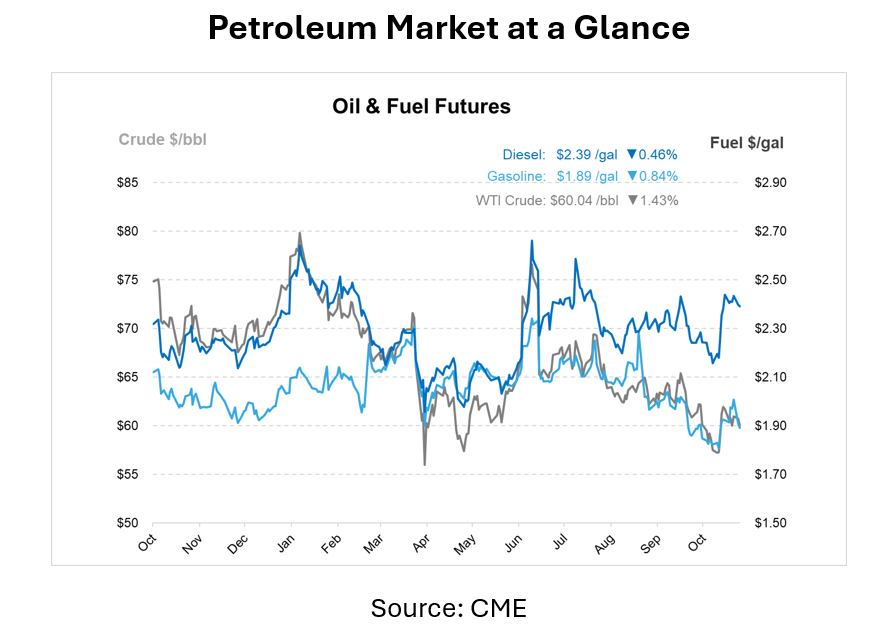

Crude Dips Below $61 as Dollar Strengthens and Demand Weakens

Crude oil prices are continuing their decline this week as global supply builds, manufacturing activity slows, and a stronger U.S. dollar dampens investor sentiment. Prompt crude futures fell by over $1 per barrel on Tuesday, extending a downward trend fueled by weakening demand signals and shifting OPEC+ production strategies. Brent crude futures are trading around $63.91 per barrel, while U.S. West Texas Intermediate (WTI) is sitting near $60—a level not seen since early summer.

Markets remain cautious following OPEC+’s decision to approve a modest production increase for December and pause output hikes during the first quarter of 2026. The pause, reportedly backed by Russia due to its difficulty in increasing exports under Western sanctions, temporarily pushed prices up earlier in the week. However, that boost quickly faded as traders refocused on macroeconomic headwinds. Manufacturing indices across Asia and the U.S. registered their weakest readings in months, reflecting softening industrial demand for energy. At the same time, the U.S. dollar reached a three-month high, making dollar-denominated commodities more expensive for foreign buyers and pressuring global oil consumption.

In the U.S., refining and production trends continue to shape price dynamics. The Energy Information Administration (EIA) reported record-setting U.S. crude output of 13.64 Mbpd for late October, showing just how resilient American production remains despite lower rig counts. Baker Hughes reported that the number of active U.S. oil rigs fell by six last week to 414, the lowest in seven weeks, suggesting slower drilling activity ahead even as production remains historically strong.

The U.S. government continues efforts to rebuild the Strategic Petroleum Reserve (SPR) after heavy drawdowns in 2022 and 2023. In October, the Department of Energy added 2.6 million barrels to the SPR, marking the third consecutive monthly build and the largest increase since May. Total reserves now stand at 409.6 million barrels, the highest level since September 2022, although they are still nearly 37% below their 2020 peak. The Biden administration initiated the refill program in mid-2023, and the effort is continuing under the Trump administration, which recently announced plans to purchase another 1 million barrels for delivery later this year.

Meanwhile, U.S. diesel markets are facing added strain as geopolitical factors ripple through supply chains. In Turkey, major fuel suppliers have raised diesel prices following Western sanctions on Russian energy companies, which disrupted regional flows and increased shipping costs. Domestically, diesel inventories remain tight relative to pre-pandemic levels, keeping prices elevated compared to crude benchmarks.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")