Week in Review – Refinery Outages and Global Diplomacy Keep Markets on Edge

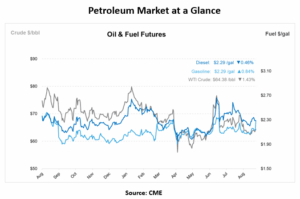

Crude is trading slightly lower this morning at $64.40/bbl but remains on track to close the day nearly $0.50 higher than last Friday. The modest gain comes amid a mix of geopolitical tensions, refinery outages, and shifting global trade flows, while U.S. economic strength and improving supply fundamentals continue to influence the outlook for both crude and refined products.

Heading into Labor Day, U.S. retail gasoline prices averaged $3.15/gal on August 25, about $0.17 lower than a year ago. The EIA projects a further drop, forecasting an 11% decline, or roughly $0.35/gal, from August through December as crude prices ease on supply growth.

Energy markets have been closely watching headlines out of Europe and Asia. Hopes for direct talks between Ukrainian President Volodymyr Zelenskiy and Russian President Vladimir Putin faded after German Chancellor Friedrich Merz said such a meeting was unlikely, despite earlier speculation from the U.S. At the same time, Putin is scheduled to meet with Indian Prime Minister Narendra Modi and Chinese President Xi Jinping to discuss energy partnerships.

Oil trade flows also made news, with Indian refiners increasing purchases of U.S. crude, particularly WTI, as its pricing has been more attractive compared to alternatives. Meanwhile, India’s imports of Russian crude are projected to rise in September by up to 300,000 bpd compared with August, even as the U.S. applies pressure for reductions.

On the refining side, Mexico’s Minatitlán refinery restarted operations this week, while the country’s large Dos Bocas facility remains offline. In Russia, refinery runs dropped to their lowest levels in three years due to repeated Ukrainian drone strikes, reducing crude processing by 700,000 bpd. Ukraine also claimed strikes on refineries in Samara and Krasnodar, further underscoring the vulnerability of Russian energy infrastructure.

The U.S. Energy Information Administration (EIA) reported a crude draw of 2.4 million barrels last week, larger than the 1.9 million barrel draw expected. Gasoline and distillates also fell, with distillate inventories now sitting about 15% below their five-year average.

Even so, demand for refined products remains below pre-pandemic benchmarks. Gasoline demand averaged 8.9 million bpd in April 2025 compared with 9.4 million bpd in April 2019, reflecting efficiency gains in the vehicle fleet. Distillate demand was also lower, partly due to growing biofuels substitution, while jet fuel use continues to lag 2019 levels despite strong travel activity.

The U.S. economic data added some support, with Q2 GDP revised up to 3.3% and jobless claims trending steady. Still, concerns over tariffs and global trade weighed on sentiment. President Trump raised pressure on India by implementing a 25% tariff hike on Indian exports in retaliation for its Russian crude purchases, while also warning Russia of “massive sanctions” if a peace agreement with Ukraine cannot be reached soon.

In Europe, the UK, Germany, and France triggered a 30-day process to reinstate sanctions on Iran after stalled nuclear negotiations. At the same time, the EU is preparing a 19th sanctions package against Russia aimed at blocking third-country circumvention.

Looking ahead, Goldman Sachs Research reiterated its forecast that prices are likely to hold near current forward levels through 2025 but could weaken in 2026 as OECD stock builds accelerate, unless China accelerates storage builds or Russian output falters.

Prices in Review

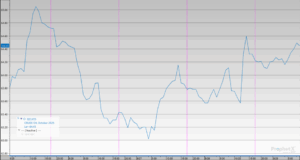

Crude prices moved modestly through the week, starting at $64.53 on Monday and sliding to $63.66 by Wednesday, the week’s low. Prices edged up to $63.76 on Thursday before opening Friday at $64.40. Overall, crude prices declined by $0.13, or 0.20%, for the week.

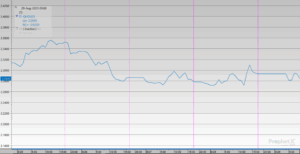

Diesel prices moved steadily lower over the week, opening at $2.3461 on Monday and easing to $2.2917 by Wednesday. The downward trend continued into Friday, when diesel reached $2.2845, the week’s low. Overall, diesel fell $0.0616, or 2.63%, for the week.

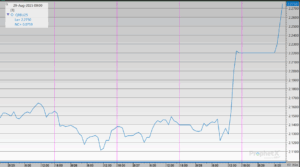

Gasoline prices saw some swings during the week, starting at $2.1575 on Monday and dipping to $2.1280 on Tuesday, with a further slide to $2.1222 on Thursday, the week’s low. By Friday, prices rebounded to $2.2750, the week’s peak. Overall, gasoline gained $0.1175, or 5.44%, for the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")