Week in Review – Prices Jump as Diesel Tightens and Sanctions Bite Fuel Markets

Fuel markets were anything but quiet this week, as a wave of geopolitical moves and supply-side shakeups sent ripples through prices. While crude oil surged more than $1/bbl on Friday morning, the weekly trend is still slightly down, pulled lower by a midweek surprise build in inventories and lingering global economic uncertainty. Behind the volatility is fresh EU sanctions on Russian fuel, tighter diesel inventories, and mounting concerns over regional supply bottlenecks—all fueling a week of tension across energy markets.

The most pivotal market driver came from Europe, where the EU introduced its 18th sanctions package against Russia. The new measures include lowering the G7 price cap on Russian crude to $47.60 per barrel and banning imports of petroleum products refined from Russian oil. While the ban excludes imports from allies like the U.S., Canada, and Norway, it could still strain global diesel supply, particularly in Europe. Gasoil futures responded with a sharp 15% spike—reaching their highest level since February 2024—highlighting growing concerns over diesel and jet fuel availability. India, which has been a major exporter of Russian-refined fuels to the EU and UK, may no longer be a reliable supplier under the new restrictions.

The real impact of the sanctions may be limited. Enforcement remains a challenge without backing from the United States. President Trump has hinted at further sanctions against buyers of Russian exports but has yet to formalize any actions. As a result, markets are cautiously watching for follow-through on sanctions policy, which could reshape global supply chains in the months ahead.

Meanwhile, other supply-side developments added to the market’s volatility. Saudi Arabia’s seaborne crude exports jumped to 6.43 Mbpd in early July, marking a 16-month high and signaling robust output from one of the world’s top producers. Conversely, China’s diesel exports plummeted nearly 60% year-over-year in June, reflecting shifting priorities and reduced availability of refined products for the global market.

Iraq moved closer to restarting crude exports from the Kurdish region, approving a plan to transfer 230,000 bpd to Baghdad. However, conflicting reports and unresolved contractual details mean a full resumption remains uncertain. If finalized, the deal could restore a critical flow of crude to the global market after a two-year hiatus.

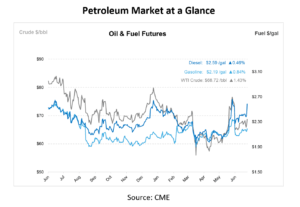

In the U.S., fuel markets were further pressured by an unexpected build in product inventories. This surprise triggered a sharp price drop midweek, even though diesel inventories remain below ideal levels. Diesel futures continued to trade at a roughly 25-cent premium to gasoline—an unusual spread for peak summer driving season—indicating lingering concerns about tight distillate supply. Notably, the EIA’s reported diesel stocks exclude growing volumes of biodiesel and renewable diesel, which are especially relevant in markets like California.

Looking ahead, refinery utilization remains a key variable. Continued rates in the mid-90% range will be essential to replenish the supply. However, unplanned outages at East Coast refineries have contributed to lower inventories in PADD 1 and could lead to tighter conditions along the Colonial Pipeline corridor. While not alarming yet, regional supply disruptions could create challenges.

Prices in Review

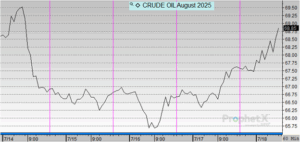

Crude prices opened the week at $68.68 and faced moderate declines through midweek. Prices dipped to $66.86 on Tuesday and continued to edge lower, reaching $66.60 by Thursday. A slight uptick on Friday brought crude up to $67.60. Overall, crude fell by $1.08 per barrel, a week-over-week decrease of approximately 1.57%.

Diesel prices opened at $2.4642 on Monday and saw volatility throughout the week. The lowest point came on Tuesday, when prices dropped to $2.3807. Prices reversed slightly midweek, reaching $2.4130 on Wednesday and dipping again on Thursday to $2.3916. On Friday, diesel jumped to $2.4726, closing the week higher.

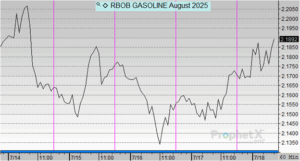

Gasoline prices opened at $2.1958 on Monday and trended downward early in the week, hitting a low of $2.1472 on Thursday. A slight reversal followed, with prices climbing to $2.1749 on Friday. Despite some midweek volatility, gasoline ended the week down $0.0209 per gallon, reflecting a 0.95% decrease overall.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")