Biofuels Production Shifts as RFS Requirements Outpace Incentives

The U.S. biofuels industry is facing a supply challenge, driven by recent changes to federal incentives and ongoing uncertainty in the Renewable Fuel Standard (RFS) policy. Industry groups representing the majority of U.S. fuel retailers warn that, without clear and consistent policy signals, investment in production capacity and infrastructure risks stagnation, potentially undermining both environmental goals and the economic benefits of a robust domestic biofuels sector.

The Renewable Fuel Standard

The Renewable Fuel Standard (RFS) is a federal program administered by the U.S. Environmental Protection Agency (EPA) that promotes the use of renewable fuels in the nation’s transportation fuel supply. Established by the Energy Policy Act of 2005 and expanded by the Energy Independence and Security Act of 2007, the RFS sets annual volume requirements for renewable fuels such as ethanol, biodiesel, and advanced biofuels.

Its primary goals are to reduce greenhouse gas emissions, expand the renewable fuels sector, and decrease U.S. reliance on imported oil. The EPA is responsible for setting and enforcing the renewable volume obligations (RVOs) for fuel producers and importers. Learn more about RVOs here.

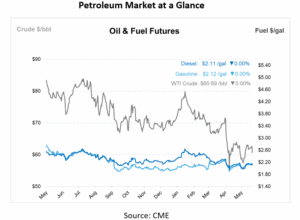

Impact of Expiring Tax Credits

For years, the $1-per-gallon Blender’s Tax Credit provided essential financial support to biofuel producers, helping stabilize prices and encourage investment. The expiration of this credit at the end of 2024, combined with the introduction of the less robust Section 45Z Clean Fuel Production Tax Credit, has shaken industry confidence. As a result, many biodiesel and renewable diesel facilities have scaled back production or shut down entirely, with states like Iowa—historically a leader in biodiesel production—now facing the potential loss of most of their capacity this year. The fallout is critical: Total renewable diesel and biodiesel volumes have dropped by more than 50% in some cases, leading to higher fuel prices and increased market volatility.

If RFS blending obligations remain high while economic incentives diminish, producers may struggle to supply enough renewable fuel to meet mandated volumes. This scenario risks non-compliance with federal requirements, further price spikes, and potential shortages across the fuel supply chain.

Decline in Production Volumes and Market Strain

A decline in biofuel production is creating significant challenges throughout the U.S. fuel supply chain. Additionally, trade reports suggest that more than 20 biofuel production plants—representing nearly 15% of the U.S. biofuels market—could close or idle in 2025, potentially reducing annual capacity by as much as 750 million gallons.

The resulting contraction in production volumes, combined with facility closures and reduced investment, is straining market stability. These disruptions could drive up diesel prices and introduce greater volatility for producers and consumers alike.

Calls for Policy Certainty and Collaboration

Fuel retailers and sustainability advocates continue to support policies that strengthen U.S. energy independence and ensure a stable fuel supply. They also argue that extending the biodiesel blenders’ tax credit would bring much-needed certainty to the market and help prevent further disruptions. Without such action, they urge the EPA to consider current market conditions when setting future renewable volume obligations, cautioning that unrealistic mandates could destabilize the sector and burden consumers.

Without swift policy intervention—whether through Congressional action or regulatory flexibility—supply challenges are likely to worsen, threatening the renewable fuels market nationwide.

Want to stay ahead of the curve and keep up with the latest developments in the oil and gas industry? Join the conversation on FUELSCast—available on your favorite podcast platform. Stay informed, stay prepared.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.