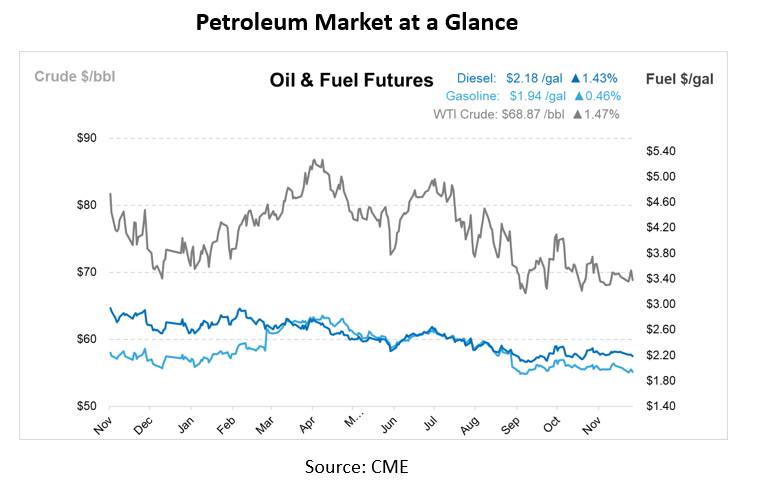

Goldman Sachs Sees Crude Rally in 2025 Despite Elevated Global Output

Goldman Sachs has expressed a moderately bullish outlook on Brent crude for the first quarter of 2025, projecting prices to climb to $76 per barrel. This optimism comes despite significant recent increases in crude production from Iran, Kazakhstan, and Canada, which have pressured oil benchmarks in recent weeks. The bank also forecasts potential turbulence in 2026, citing trade policies as a potential catalyst for price declines.

Global Production Trends Impacting Markets

Elevated production levels in several key regions are central to the current challenges facing crude benchmarks:

Iran – Crude production in Iran has surged to a six-year high of 3.6 million barrels per day (b/d). Goldman attributes this to possible “front-loading” by Iran in anticipation of policy shifts under the next U.S. administration. Analysts suggest that Iran may be aiming to mitigate the potential impact of sanctions or trade restrictions that could emerge early next year.

Kazakhstan — Recently, Output in Kazakhstan has jumped by 12% following the completion of field maintenance. This boost in supply has further contributed to the global surplus.

Canada – Alberta’s liquid production increased by a robust 13% in October, with further growth on the horizon. The Canadian Association of Energy Contractors predicts a 7% rise in drilling activity for 2024, signaling continued expansion in Canadian crude supply.

OPEC+ Likely to Extend Cuts

OPEC+ is expected to play an important role in stabilizing prices. Goldman anticipates that the coalition will announce an extension of its production cuts during its upcoming meeting. These cuts, initially set to expire in January 2025, are likely to be extended through the first quarter. The move aims to counterbalance the oversupply from non-OPEC producers and support market recovery.

Price Dynamics and Inventory Draws

Despite recent supply challenges, Goldman remains optimistic about a near-term rally. The bank highlights a decline in OECD commercial oil inventories, which are down by 11 million barrels year-over-year. Additionally, global inventory draws have averaged 600,000 b/d over the past 90 days, indicating a tighter market than headline production figures might suggest.

However, market sentiment, as reflected in managed money positions for Brent futures, remains subdued. Goldman notes that net length for crude positions is in the historically low 5th percentile, signaling weak speculative interest. Analysts suggest that the shift of speculative investments toward sectors like cryptocurrency and technology may have reduced crude’s appeal as a high-yield asset class.

Impact of US. Tariff Policies

Looking beyond 2025, Goldman warns of significant risks tied to potential U.S. trade policies under the Trump administration.

Canadian Crude Tariff – A proposed 25% tariff on Canadian crude imports could have a dramatic impact, driving Western Canadian Select (WCS) prices below $40 per barrel in 2026. This marks a sharp decline from its current $56–$57 range and could pressure Canadian producers reliant on U.S. markets.

Universal Tariff Excluding Oil – A broader 10% tariff policy exempting crude could also harm the energy sector. Goldman predicts a “substantial negative effect” on U.S. crude and gasoline prices, stemming from reduced aggregate demand in an already cautious economic environment.

Long-Term Outlook

Goldman’s analysis underscores the complex interplay of geopolitical, economic, and market forces shaping the industry. While a Brent crude rally to $76 per barrel is expected in the first quarter of 2025, the bank remains cautious about 2026, with potential price declines fueled by increasing supply and trade tensions.

This article is part of Daily Market News & Insights

Tagged: 2025, Crude Rally, Global Output

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")