Week in Review – Ukraine Peace Talks and IEA Demand Cut Shape Oil Price Direction

Oil markets this week reacted to renewed diplomatic activity, with the Kremlin confirming that a fresh round of peace talks on Ukraine is scheduled for next week, keeping conflict risk in focus. Meanwhile, energy fundamentals took center stage as the International Energy Agency cut its 2026 global oil demand growth forecast and highlighted a looming surplus, reinforcing the tension between supply realities and geopolitical risk that continues to influence crude markets.

Russian authorities have announced that the next round of peace negotiations on Ukraine will take place next week. While no breakthrough has been announced, the continuation of talks signals ongoing diplomatic engagement between Moscow and Washington. A Kremlin spokesperson also acknowledged discussions around bilateral trade and economic cooperation but noted that meaningful progress is unlikely until the conflict is resolved.

The International Energy Agency trimmed its 2026 global oil demand growth forecast to 850,000 bpd. That projection is down from 930,000 bpd previously. The agency cited economic uncertainty and higher crude prices as headwinds, reinforcing the idea that elevated prices can ultimately curb consumption. For context, OPEC+ continues to project stronger growth of roughly 1.4 Mbpd in 2026, underscoring a widening gap between producer and consumer outlooks.

Even more notable was the IEA’s projection that global supply could exceed demand by 3.73 Mbpd in 2026, which is nearly 4% of total world consumption. While January outages temporarily tightened balances, the broader trajectory still points toward a supply surplus. Supply fell by 1.2 Mbpd last month to 106.6 Mbpd as extreme winter storms slashed output across the U.S. and Canada and export disruptions constrained flows from Kazakhstan, Russia, and Venezuela. The U.S. alone saw an estimated 860,000 bpd curtailed due to frigid temperatures and infrastructure shutdowns.

Looking ahead, the agency expects much of that lost production to return in the coming months. Global supply growth for 2026 is now forecast at 2.4 Mbpd, only slightly below last month’s estimate and still well above projected demand growth. Production gains are expected from both OPEC+ and non-OPEC+ countries, including the U.S., Guyana, and Brazil. Meanwhile, OPEC+ output in January stood at 43.3 Mbpd, well above the group’s implied call on crude for the first half of the year.

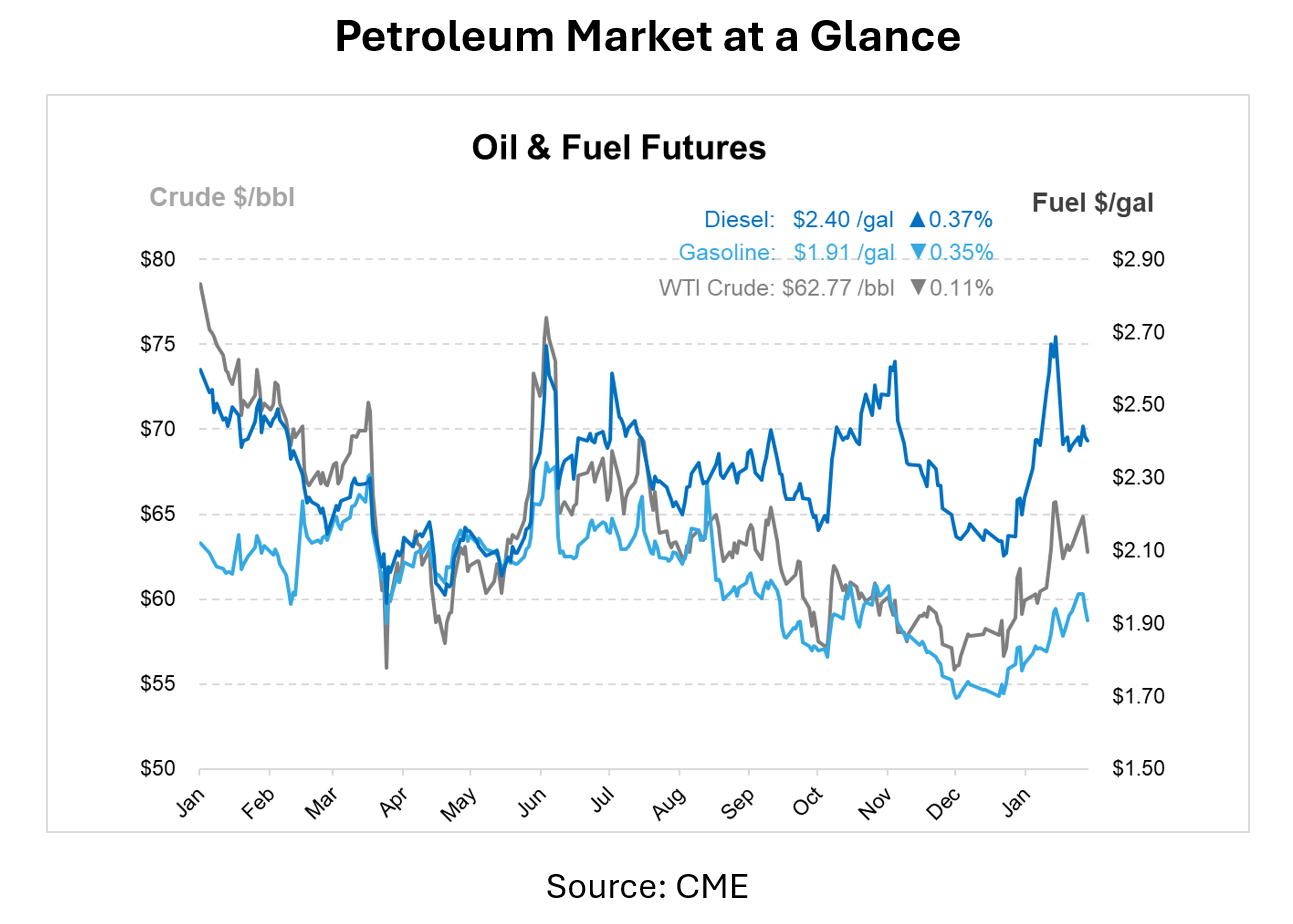

On the U.S. data front, the Energy Information Administration reported an 8.5 million barrel crude build for the week ended February 6, well above expectations. Cushing inventories rose by 1.1 million barrels. Gasoline stocks increased by 1.2 million barrels, while distillates drew by 2.7 million barrels. Crude inventories remain about 3% below the five-year average, gasoline stocks are 4% above, and distillates are 4% below, offering a generally comfortable supply picture.

Adding another layer, Saudi Arabia is expected to boost exports to China to multi-year highs in March after cutting official selling prices to Asia for a fourth consecutive month, signaling competitive positioning amid softer demand expectations.

Prices in Review

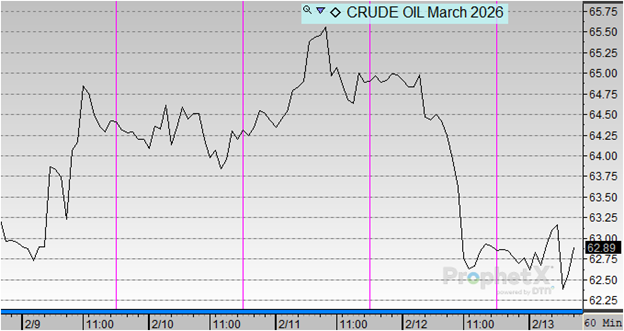

Crude opened the week at $62.99 on Monday before climbing to $64.44 on Tuesday. Prices eased slightly on Wednesday to $64.20, then rose again on Thursday to reach the weekly high of $64.87. However, those gains were short-lived, with crude retreating to $62.99 on Friday. Overall, crude prices ended the week flat, with no change from Monday’s open.

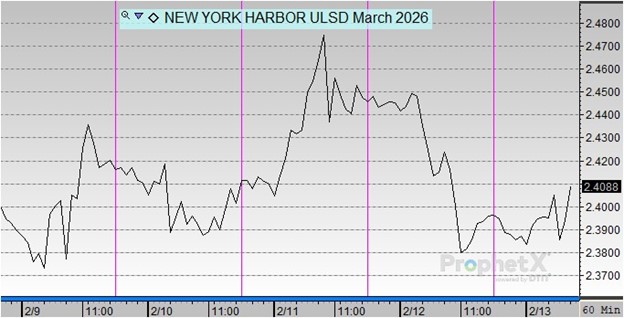

Diesel prices moved higher early in the week before easing slightly into Friday. Diesel opened the week at $2.3869 on Monday and climbed to $2.4216 on Tuesday. Prices dipped modestly on Wednesday to $2.4012, then rose on Thursday to a weekly high of $2.4513. Those gains were partially erased on Friday, with diesel settling at $2.3975. Overall, diesel prices increased by $0.0106 over the course of the week, representing a 0.44% gain.

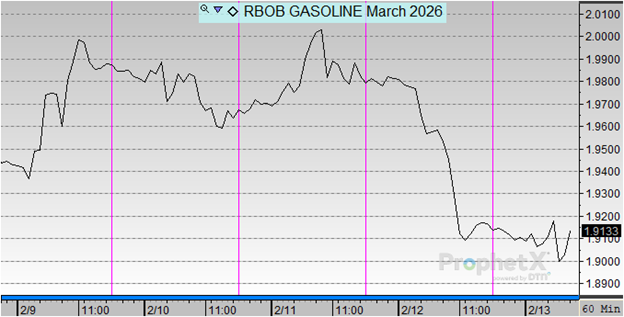

Gasoline opened the week at $1.9460 on Monday before climbing to $1.9881 on Tuesday. Prices eased on Wednesday to $1.9670, then ticked higher again on Thursday to $1.9840. However, those gains were erased on Friday, with gasoline opening at $1.9170. Overall, gasoline prices declined by $0.0290 over the course of the week, representing a 1.49% decrease.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")