Week in Review – Refinery Runs Strengthen Supply as Geopolitical Risks Compete with Growing Surplus

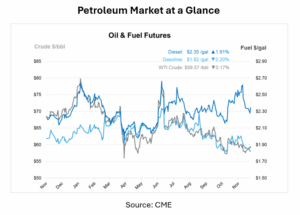

U.S. fuel markets entered December with a mix of improving domestic supply, geopolitical uncertainty, and shifting macroeconomic expectations. Crude is ending the week with prices just shy of $60/bbl, while diesel is up 4 cents to $2.35 and gasoline is down 3 cents to $1.82. US markets are also anticipating a Fed rate cut at next week’s Federal Reserve meeting.

One of the most significant developments this week has been the strength in refinery utilization. U.S. facilities operated above 94%, approaching the seasonal ceiling and contributing to increased builds in both gasoline and diesel inventories. While diesel demand increased during recent winter weather systems, elevated refinery output helped blunt the impact. Even so, national diesel stocks remain below last year’s levels, and the East Coast continues to experience pockets of tightness. These pockets are manageable for now, but still a key watch point for winter operations. Historically, utilization peaks in early December before easing in late December and January due to holiday slowdowns, weather, and turnaround preparation, meaning today’s strong production window may not last long.

Globally, crude markets spent the week navigating competing influences. On the geopolitical front, Ukraine intensified its drone campaign against Russian refining and export assets, striking the Druzhba pipeline, along with refineries that have collectively pushed Russian throughput roughly 335,000 bpd lower year-over-year. These disruptions reduce Russia’s ability to supply refined products, particularly gasoline, tightening balances and creating upward pressure on distillate markets. At the same time, stalled U.S.–Russia peace discussions lowered expectations that a negotiated settlement would bring additional Russian barrels back into an already saturated market.

But alongside these geopolitical tensions, the broader supply landscape remains robust. Saudi Arabia lowered the January price of its Arab Light crude to Asia to the weakest level in five years, which proves expectations of plentiful global supply heading into early 2026. Domestically, the latest EIA report showed a 574,000-barrel crude build driven by strong refinery runs, reinforcing a narrative of adequate U.S. supply even as winter heating demand rises. Fitch Ratings echoed this view, revising its 2025–2027 price assumptions downward on the expectation that worldwide production growth will exceed demand.

Macro-economic expectations added another layer of complexity. Markets are increasingly anticipating a Federal Reserve rate cut, which could stimulate economic activity and, in turn, fuel demand. For fleets managing large fuel budgets, the possibility of stronger demand intersecting with already-tight distillate markets remains an important scenario to plan for.

In downstream logistics, Colonial Pipeline requested a rehearing after regulators rejected its proposed changes to gasoline shipment specifications, which are adjustments the company argues would improve safety, efficiency, and capacity on the system. With U.S. gasoline consumption exceeding 8.3 Mbpd, the outcome may influence future supply patterns along the East Coast.

Prices in Review

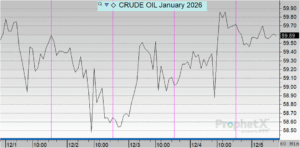

Crude prices opened the week at $58.96 on Monday and showed modest day-to-day movement. Prices edged higher to $59.52 on Tuesday before slipping to the weekly low of $58.65 on Wednesday. By Thursday, crude increased slightly to $59.09, and this morning opened at $59.70, the highest level of the week. Overall, crude increased by $0.74, marking a 1.26% gain week-over-week.

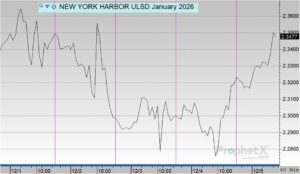

Diesel prices opened the week at $2.3198 on Monday and saw moderate fluctuations. Prices ticked up to $2.3441 on Tuesday, the weekly high, before retreating midweek. Wednesday brought the sharpest decline, with diesel falling to $2.3037, followed by a slight dip to the weekly low of $2.3015 on Thursday. This morning, diesel opened at $2.3221, essentially returning to Monday’s level. Overall, diesel increased by $0.0023, a 0.10% gain for the week.

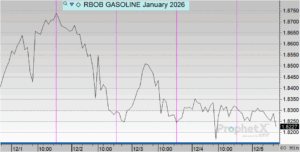

Gasoline prices opened at $1.8261 on Monday and rose on Tuesday, reaching the weekly high of $1.8708. Prices then eased midweek, falling to $1.8332 on Wednesday and edging slightly lower to $1.8268 on Thursday, marking the weekly low. This morning, gasoline opened at $1.8321, ending the week just above Monday’s starting point. Overall, gasoline increased by $0.0060, reflecting a 0.33% gain for the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")