Oil Prices React to India-Russia Trade and Global Supply Shifts

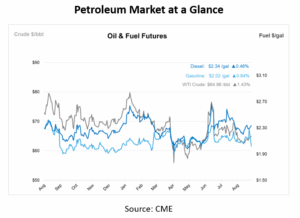

Oil Markets entered the post-Labor Day trading week with higher prices and lower trading volumes. West Texas Intermediate (WTI) rose by $1.80 per barrel on Tuesday morning, driven by supply-side disruptions, diplomatic developments, and market speculation. The price rally follows a quiet holiday weekend and reflects the market’s sensitivity to geopolitical news and tightening global supply.

One of the key drivers remains India’s ongoing purchase of discounted Russian crude. Despite sustained pressure from the U.S. to reduce its reliance on Russian barrels, India continues to secure Urals crude at a $3 – $4 discount to Brent. India’s Oil Minister Hardeep Puri defended the move, saying the country has not broken any rules and its purchases have helped prevent a global price spike. At the same time, Saudi Arabia and Iraq halted shipments to a major Indian refinery recently sanctioned by the European Union, putting further strain on regional flows.

In the Middle East, Iraq reported a 7% increase in crude exports during August, reaching the highest level since December 2023. This increase is part of OPEC+’s broader move to ease earlier production cuts. Meanwhile, Syria restarted crude exports for the first time in years, shipping 600,000 barrels per day of heavy crude after the U.S. lifted sanctions to support the country’s fragile economy.

Back in the U.S., legal developments could reshape future trade policy. A federal court upheld an earlier ruling that blocked tariffs imposed under the International Economic Emergency Powers Act, though the decision will not take effect until October 14. If the case moves to the Supreme Court, these tariffs could remain in place until mid-2026. This legal uncertainty may prompt changes to how tariffs are applied and could have implications for global commodity flows.

Macroeconomic data from July suggests slowing momentum in the U.S. economy. Core PCE, the Federal Reserve’s preferred measure of inflation, rose 0.27% month-over-month and 2.88% year-over-year. Personal income and spending both increased modestly, while the goods trade deficit widened more than expected due to higher imports of industrial and capital goods. Goldman Sachs analysts revised their third-quarter GDP tracking estimate to 1.6%, down from 1.8%, and lowered domestic final sales estimates to just 0.6%.

Oil’s correlation with global inflation remains a topic of focus for stakeholders. According to GIR research, oil price shocks continue to influence traded inflation rates in the U.S., Europe, and the UK. With expectations of a supply surplus on the horizon, falling oil prices could exert downward pressure on European inflation. However, the potential for a peace deal in Eastern Europe and a resurgence in Russian energy exports may create additional headwinds for inflation-linked assets.

In the physical market, U.S. crude rig activity increased slightly, rising by one rig to a total of 412. The count remains down 71 rigs year-over-year. Canada’s rig count, by contrast, fell by three rigs to 120, reflecting ongoing softness in activity compared to last year’s levels.

Meanwhile, WTI crude saw a slight reduction in net length, driven by increased short positions. Brent Crude, however, experienced a jump in long positions, suggesting growing optimism around future price movements. Gasoline and heating oil also recorded increases in speculative length, reflecting seasonal demand expectations and broader bullish positioning.

The International Energy Agency (IEA) expects global capital investment in the energy sector to reach $3.3 trillion in 2025, marking a 2% increase from 2024. This increase signals a longer-term commitment to infrastructure development across both traditional and renewable energy sectors.

This article is part of Daily Market News & Insights

Tagged: brent, crude prices, Diesel Futures, Energy Policy, global energy investment, IEA, NYMEX, Oil Market, opec, tariffs, traded inflation, WTI

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")