Oil Markets Balancing Geopolitical Tensions, Rising Supply, and Slowing Demand

Crude prices slipped by over 50 cents this morning as markets weighed a mix of geopolitical developments and shifting supply-demand dynamics. President Trump’s decision to extend the tariff truce with China for 90 days eased trade war concerns, offering temporary relief to markets. The pause follows a third round of negotiations in less than three months, but Trump defined expectations for his upcoming meeting with Russian President Vladimir Putin, calling it a “feel-out” session. Ahead of the summit, European leaders and Ukraine’s President Zelenskiy plan to discuss strategies for pressuring Russia and advancing peace talks.

Refining and export markets are also adjusting to new trade realities. Indian refiner Nayara Energy is operating at about 70% capacity, its lowest-ever crude intake, following recent EU sanctions, while Russia’s crude exports have declined for three straight weeks. Indian refiners are shifting toward non-Russian cargoes in anticipation of a new 25% U.S. tariff on Indian exports, though the impact on Russian flows may not be felt for weeks. Despite these developments, Brent and WTI implied volatility has eased to a two-week low, signaling calmer short-term sentiment. In the chart below, implied volatility represents the market’s expectations for how much crude prices will fluctuate in the near future. Spikes like the sharp jump to 68% in mid-June 2025 indicate heightened uncertainty and risk in the market, often triggered by geopolitical events such as the Iran nuclear conflict.

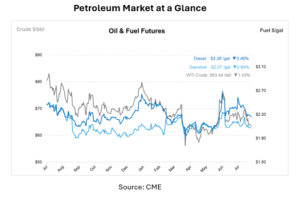

In the broader market, U.S. petroleum production remains at record highs, averaging over 20.5 Mbpd in the first five months of 2025. This resilience comes even as OPEC+ unwinds production cuts in an effort to reclaim market share. Still, mid-June tensions over Iran’s nuclear program briefly spiked Brent prices to $80/bbl before easing after a ceasefire. The EIA now forecasts Brent to average $66/bbl in the second half of 2025, nearly $5/bbl higher than last month’s estimate, before falling to $58/bbl in 2026 as rising inventories weigh on prices.

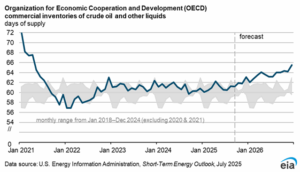

Global oil demand is expected to rise modestly, according to the most recent EIA Short Term Energy Outlook, with a projected 0.8 Mbpd increase in 2025 and 1.1 Mbpd in 2026, driven almost entirely by non-OECD consumption in Asia. On the supply side, both OPEC+ and non-OPEC+ producers, particularly the U.S., Brazil, Canada, and Guyana, are set to expand output by 1.8 Mbpd in 2025 and 1.1 Mbpd in 2026. The imbalance between rising supply and moderate demand growth is likely to swell OECD inventories to 66 days of supply by the end of 2026, well above historical norms, limiting the potential for sustained price gains.

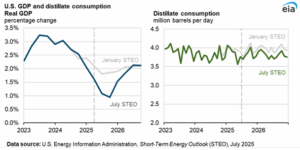

In the U.S., crude oil production is forecast to edge down from nearly 13.5 Mbpd in April 2025 to 13.3 Mbpd by late 2026, pressured by an expected 22% drop in WTI prices to $53/bbl. Lower prices are curbing drilling and completion activity, with the first half of 2025 seeing the fewest well completions since 2021. At the same time, U.S. distillate consumption is slipping on weaker economic growth, falling by 30,000 bpd in the second half of 2025 versus a year earlier. Industrial activity, manufacturing output, and trucking demand have all softened, though modest distillate demand growth is projected for 2026.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")