Week in Review – Prices Hit Two-Month Lows on Tariff Threats and Demand Concerns

Fuel markets endured a volatile week, with prices pressured by geopolitical uncertainty, soft economic indicators, and shifting global trade flows. Both West Texas Intermediate (WTI) and Brent crude futures closed Thursday at their lowest levels since early June, before the mid-June flare-up between Israel and Iran.

Speculation over a potential meeting between U.S. President Donald Trump and Russian President Vladimir Putin fueled talk of possible sanctions relief on Russian oil, though any output increase would take time and face steep political hurdles. The U.S. has escalated trade tensions, imposing a 25% tariff on goods from India over its Russian oil imports and signaling similar action against China, the largest buyer. Aimed at cutting Moscow’s war revenue, the move risks straining relations with both countries, disrupting up to 2% of global oil supply, and pushing Brent crude into the $80s or higher. Such disruptions could spike fuel prices and fuel inflation. Russia could also retaliate by closing export routes like the CPC Pipeline, while its adaptability to past sanctions raises doubts that tariffs will change Putin’s stance.

Economic signals have done little to calm market nerves. July’s weak U.S. labor report, combined with downward revisions to previous months, has amplified concerns over slowing domestic demand. At the same time, second-quarter nonfarm productivity beat expectations at 2.4%, with annual growth at 1.3%, but unit labor costs rose more than forecast, suggesting underlying inflationary pressures. Initial jobless claims edged up to 226,000, slightly above expectations.

Between April and June, OPEC production rose by 540,000 bpd, short of its 730,000 bpd pledge, as Iraq and Russia cut output to offset past overproduction and Kazakhstan hit capacity limits. In July, output increased by 270,000 bpd to 27.38 Mbpd, led by the UAE and Saudi Arabia, though gains were partially offset by Iraq’s additional cuts and Kurdish oilfield disruptions. The UAE added about 100,000 bpd, still below quota, while Iraq reduced volumes under compliance pressure. Some outside estimates, including from the IEA, suggest Iraq and the UAE may be producing above reported levels.

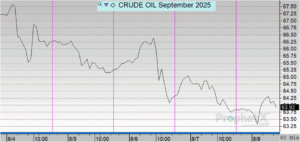

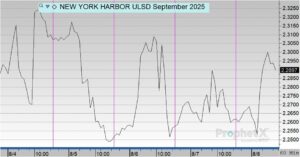

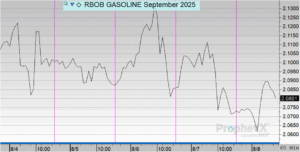

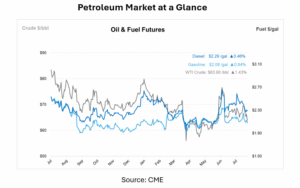

Prices in Review

Crude prices opened the week at $66.85 on Monday and trended lower over the following days. Tuesday saw a slight dip to $66.21, followed by a sharper drop to $65.15 on Wednesday. The downward momentum continued into Thursday, with prices falling to $64.36, before closing the week at $63.85 on Friday. Overall, crude fell $3.00/bbl, or 4.49%, for the week, marking its steepest weekly loss since late June.

Diesel prices opened at $2.28 on Monday and saw modest fluctuations throughout the week. Prices rose slightly to $2.3070 on Tuesday before slipping to the weekly low of $2.2529 on Wednesday. A mild reversal followed, with diesel climbing to $2.2622 on Thursday and holding nearly steady at $2.2608 on Friday. Overall, diesel posted a small weekly gain of $0.0192/gal, or 0.84%.

Gasoline prices opened at $2.1025 on Monday and declined steadily throughout the week. Tuesday saw a slight dip to $2.0992, followed by $2.0900 on Wednesday and $2.0877 on Thursday. The week closed at $2.0774 on Friday, marking the lowest level of the week. Overall, gasoline fell $0.0251/gal, or 1.19%, for the week.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")