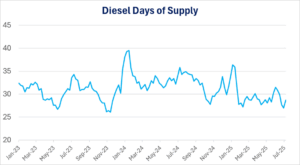

Inventory Concerns Take Center Stage as Diesel Days of Supply Drop Below 30

Diesel supply concerns are rising to the forefront of market headlines as U.S. inventories remain unusually tight for this time of year. For the third straight week, diesel days of supply have hovered between 27 and 28, a few days below the 30-day threshold typically associated with a well-supplied market. These levels are especially concerning in mid-summer, a period when inventories are expected to build in preparation for the winter season. If this winter proves to be colder than average, today’s inventory shortfalls could translate into significant price spikes down the line. The market is already reacting, with the NYMEX heating oil crack spread to WTI jumping to nearly $38/bbl — its highest point since February.

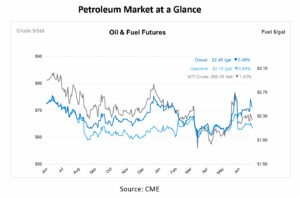

WTI crude oil prices dipped by more than $0.70/bbl this morning, ahead of today’s August contract expiry. The move comes after global geopolitical shifts. India urged caution in applying secondary sanctions on Russian oil, prioritizing energy security, while China strongly objected to the EU’s latest sanctions, warning of broader trade and financial fallout. Meanwhile, Iran has signaled a willingness to resume nuclear talks with the U.S., and China’s refining sector is showing tentative signs of recovery, with some previously bankrupt refiners seeking crude import quotas. These developments, paired with an already tight diesel market, are creating a volatile backdrop heading into the second half of the year.

On the East Coast (PADD 1), where NYMEX diesel futures contracts are settled, inventory concerns are even more acute. A mix of unplanned refinery outages, sanctions-related trade disruptions, and resilient demand has led to persistently low inventory levels. Relief hinges on increased supply flows from the Gulf Coast or a weakening in demand. The diesel futures curve is in steep backwardation, meaning future prices are lower than current prices, which encourages quick turnover rather than storage.

Looking ahead, refinery utilization is expected to remain in the low-to-mid 90% range. If exports, which have remained strong, begin to ease, refiners could make up ground in restocking inventories. The futures market is already responding to this imbalance, with diesel trading at a premium of 40 cents over gasoline — a clear signal that refiners should be maximizing distillate production. However, any disruption to refining output, such as from hurricanes or geopolitical instability, could quickly deepen supply tightness.

Several “known unknowns” will shape the diesel market outlook in the coming months: economic shifts that influence demand, escalation of global conflicts that affect supply chains, and unpredictable winter weather.

This article is part of Daily Market News & Insights

Tagged: Diesel Supply, U.S. inventories

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.