OPEC Bets on Growth as Sanction Fears Rattle Oil Markets

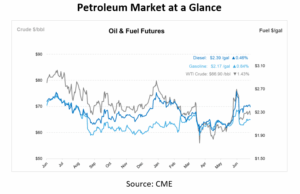

Oil prices remained mostly unchanged on Tuesday morning, following a turbulent Monday session marked by geopolitical uncertainty and shifting market dynamics. Investor focus centered on U.S. President Donald Trump’s warning of potential 100% tariffs on countries buying Russian oil, such as China and India, if Russia does not end its war in Ukraine within 50 days. While the threat initially fueled fears of tighter global supply, the extended timeline helped calm markets in the short term. Still, with tensions simmering and supply chains vulnerable to disruption, uncertainty continues to weigh on the outlook.

Despite the current state of prices, the geopolitical backdrop remains uncertain. If sanctions are implemented, they could severely disrupt Russian oil flows, particularly to large importers like China, India, and Turkey, reshaping global supply chains and potentially tightening the market. Meanwhile, a drone attack temporarily halted production at the Sarsang oilfield in Iraqi Kurdistan, highlighting ongoing risks to oil infrastructure in politically unstable regions. Although operations have resumed, the incident underscores the market’s vulnerability to sudden supply shocks.

On the supply side, China’s refining sector saw a strong rebound in June, with output reaching 15.2 Mbpd—the highest level since September 2023. This uptick followed seasonal maintenance closures and reflects a push to capitalize on improving margins, especially for fuels like diesel. Additionally, Kazakhstan reaffirmed its commitment to OPEC+ production quotas, although national interests will continue to influence its output levels, according to Prime Minister Olzhas Bektenov.

One of the most notable structural shifts is occurring on the demand front. China is poised to sell more electric vehicles than gas-powered ones for the first time in 2025, with EVs already comprising over half of total vehicle sales in the first six months. This signals a long-term shift in global fuel consumption patterns, even as short-term demand remains strong.

Reflecting tighter inventories and elevated supply risks, Goldman Sachs revised its Brent and WTI price forecasts for the second half of 2025 upward to $66 and $63 per barrel, respectively. However, the bank maintains a more bearish outlook for 2026, projecting that increased production and weaker demand growth could drive Brent and WTI prices down to $56 and $52 per barrel, respectively.

OPEC, for its part, remains optimistic about the global economic outlook. In its latest monthly report, the group held steady on its oil demand growth forecasts, citing better-than-expected performance in markets such as India, China, Brazil, and continued recovery in the U.S. and Eurozone. Rising travel and refinery activity are expected to support demand through the third quarter. OPEC+ also increased output to 41.56 Mbpd in June, just shy of its targeted rise, as the group shifts from prolonged production cuts to a strategy aimed at regaining market share.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")