Fuel Price Volatility Grips California Thanks to Refinery Closures and Policy Uncertainty

California’s fuel market is entering a period of heightened volatility thanks to declining demand, shrinking refinery capacity, renewable fuel regulatory uncertainty, and sharp swings in daily wholesale rack prices. Once a self-reliant refining hub, the state now faces growing dependency on fuel imports, while policy headwinds and inconsistent federal incentives complicate the energy landscape.

Fuel demand across California continues to decline as the state accelerates its transition to electric vehicles and low-carbon alternatives. However, this demand erosion has not kept pace with the rate of refinery closures. In the Los Angeles area, refiners still in operation include Marathon’s Carson/Wilmington complex, Chevron’s El Segundo plant, PBF’s Torrance refinery, and Phillips 66’s Wilmington facility. Yet Phillips 66 has announced it will cease refining operations by October 2025, joining a growing list of planned shutdowns that could reduce statewide refining capacity by nearly 20% in just one year. Valero is also teetering on the possibility of closing its Benicia facility in Northern California by 2026, citing regulatory pressure and high operational costs. The group is leaning towards closing the facility, but will leave the door open to continue its operations.

With fewer in-state refineries, California is increasingly reliant on imported fuels. Imports into the state reached a four-year high in May, with volumes nearing 279,000 bpd—largely sourced from Asia, including South Korea and China. The California Energy Commission (CEC) projects that as much as 30% of the state’s gasoline demand may need to be fulfilled through imports by 2026, especially in the northern half of the state. This growing reliance on overseas supply introduces longer lead times, higher freight costs, and additional supply chain risk, compounding price volatility at the pump.

Fuel prices in California are already reflecting these dynamics. Wholesale rack prices are exhibiting rapid, daily swings as traders react to tightening supply and unplanned refinery maintenance. In some instances, wholesale margins have jumped to more than $0.90 per gallon—more than double typical levels—fueled by reduced output and delays in replenishing supply via imports.

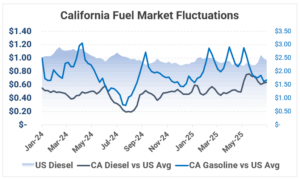

The chart above compares U.S. diesel prices (shaded background) to California diesel and gasoline premiums relative to the national average (solid lines) over an 18-month period from January 2024 through June 2025. California’s consistent price elevation above the U.S. average, along with periods of pronounced volatility, particularly for gasoline are profound.

California gasoline prices have seen sharp fluctuations throughout 2025, with several spikes exceeding a $1.00 per gallon premium over the U.S. average. Price spikes are particularly notable in March, April, and again in June 2025.

Meanwhile, California diesel prices follow a more stable trajectory but still show significant premiums compared to the U.S. average. Early 2025 saw a steady rise in the diesel spread, peaking around $0.80 per gallon in May before softening in June. This diesel premium suggests sustained pressure from tightening inventories, constrained refining capacity, and regulatory costs unique to California’s fuel market.

Complicating matters further is a wave of regulatory changes and federal policy uncertainty. The removal of the federal Blenders Tax Credit (BTC), which previously subsidized renewable diesel blending by up to $3 per gallon, has raised the cost of alternative fuels. Meanwhile, the much-anticipated 45Z tax credit—intended to incentivize low-carbon fuel production—is still undefined, stalling investment in refining upgrades. California’s own Low Carbon Fuel Standard (LCFS) continues to add pressure, and weak Renewable Identification Number (RIN) values under the federal Renewable Fuel Standard are offering little relief to producers and blenders

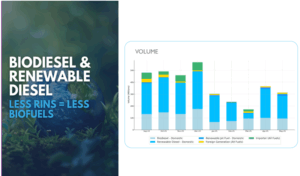

The chart above, based on EPA data, illustrates monthly volumes of biodiesel, renewable diesel, and other renewable fuel types produced or imported into the U.S. from September 2024 through May 2025. A clear downward trend emerges in January 2025, with total renewable fuel production dropping significantly compared to late 2024 levels. Notably, the steepest decline is seen in domestic renewable diesel and biodiesel output, which together account for the majority of RIN (Renewable Identification Number) generation. With RIN generation directly tied to renewable fuel output, the current trend signals a tightening biofuels market. If this trajectory continues into the summer months, RIN supply could fall even further, compounding compliance challenges for obligated parties and reducing the availability of lower-emission fuels.

Faced with growing concerns about fuel availability and price spikes, state officials appear to be reconsidering their approach. The CEC recently recommended pausing enforcement of California’s refinery profit margin cap to prevent further closures and keep existing facilities viable. Governor Gavin Newsom has also called for flexibility in regulatory oversight to safeguard the state’s fuel supply and support critical infrastructure.

In the months ahead, California’s fuel market will continue to face turbulence. The convergence of regulatory shifts, refining constraints, and increased dependence on imports creates an uncertain outlook for both suppliers and consumers. Without timely adjustments to state and federal policy—such as clarifying 45Z eligibility or expanding terminal capacity—fuel prices in California are likely to remain volatile, and potentially among the highest in the nation.

This article is part of Daily Market News & Insights

Tagged: 45Z eligibility, Blenders Tax Credit (BTC), California, California Energy Commission, fuel imports, Fuel Price Volatility, gasoline prices, Governor Gavin Newsom, Low Carbon Fuel Standard (LCFS), Refinery Closures and Policy Uncertainty, Renewable Identification Number (RIN), U.S. diesel prices

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")