Week in Review: Markets Post Steepest Weekly Drop Since 2023 Amid Fading Geopolitical Risk

This week, oil markets saw their steepest weekly decline in over two years, with both Brent and WTI crude prices falling roughly 12%.The decline reflects a broader shift away from geopolitical risk-driven pricing and a renewed focus on market fundamentals, such as inventories, trade flows, and demand trends.

Just two weeks ago, prices spiked on fears that conflict between Iran and Israel could severely disrupt global crude supplies, particularly through the Strait of Hormuz—a key chokepoint for global oil transit. Brent briefly rose above $80 per barrel during the height of the conflict, but prices quickly dropped to around $68 following the announcement of a ceasefire brokered by U.S. President Donald Trump. Despite concerns, no major supply outages occurred, leading analysts and traders to rapidly unwind the geopolitical risk premium.

According to Goldman Sachs, the likelihood of a significant disruption through the Strait of Hormuz has dropped to just 4%, down from a peak of 15% earlier this month. Options markets now reflect a 60% probability that Brent prices will remain in the $60s over the next three months, and only a 28% chance of exceeding $70. This shift takes into consideration both recent geopolitical events that failed to impact oil supplies and growing confidence in global efforts—particularly from the U.S. and China—to avoid further escalation in the region.

While prices have cooled, the U.S. Energy Information Administration data revealed notable inventory draws, especially in middle distillates, driven by strong refining activity and rising demand. In Europe, independently held gasoil stocks at the Amsterdam-Rotterdam-Antwerp (ARA) hub dropped to their lowest level in over a year. Meanwhile, Singapore’s middle distillate inventories also declined due to rising net exports. These inventory trends point to tighter short-term supply and healthy global demand.

Adding to that demand picture, China—the world’s largest oil importer—significantly ramped up its intake of Iranian crude in June, importing over 1.8 Mbpd in the first 20 days of the month. The increase came ahead of the Iran-Israel conflict and was largely driven by strong demand from independent Chinese refiners.

On the supply side, markets are eyeing the upcoming July 6 OPEC+ meeting, where a modest production increase of 411,000 bpd is anticipated. Meanwhile, in the United States, deliveries into the Strategic Petroleum Reserve (SPR) continue to lag behind schedule due to ongoing maintenance. Of the 15.8 million barrels slated for delivery in the first half of 2025, just 8.8 million have been received. The Department of Energy now expects to complete deliveries by year-end, seven months later than planned.

Broader economic signals remain mixed but generally supportive. Durable goods orders beat expectations, jobless claims declined, and Goldman Sachs revised its Q2 GDP growth estimate upward to 4.0%. In Canada, a new law passed by the Senate aims to streamline the approval process for major infrastructure projects—including pipelines and energy systems—signaling positive momentum for future energy development.

Prices in Review

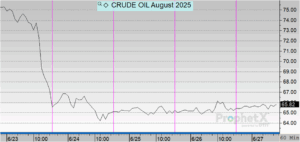

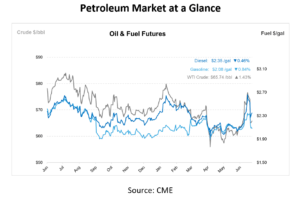

Crude prices opened the week at $78.00 but quickly came under pressure on easing geopolitical tensions and shifting market sentiment. The sharpest decline occurred on Tuesday, when prices fell to $67.74—a drop of more than $10 in a single session. The downward trend continued midweek, with crude touching a weekly low of $64.98 on Thursday. A modest increase followed on Friday, with prices ticking up slightly to $65.30. Overall, crude fell $12.70 for the week, representing a steep 16.28% decline, marking the largest weekly drop in over two years.

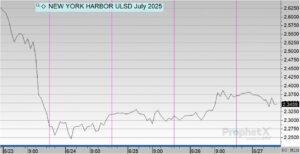

Diesel prices opened at $2.6688 on Monday and experienced significant volatility throughout the week. The steepest drop came on Tuesday, with prices falling to $2.3221—a decline of more than 34 cents. Prices stabilized slightly midweek, hovering around $2.32 on Wednesday and dipping further to $2.3089 on Thursday. A modest increase followed on Friday, with diesel opening at $2.3826. Overall, diesel prices fell by 28.62 cents this week, representing a 10.72% decline.

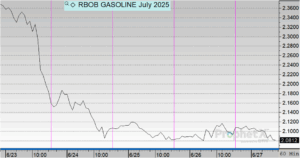

Gasoline prices opened at $2.3915 on Monday and declined steadily throughout the week. The sharpest drop occurred on Tuesday, with prices falling to $2.1950, followed by continued drops midweek, reaching a low of $2.0906 on Thursday. A slight uptick was seen on Friday, with gasoline opening at $2.1032. Overall, gasoline prices dropped 28.83 cents for the week, a decline of approximately 12.06%.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")