OPEC+ Supply Jump Shakes U.S. Light Sweet Crude Market

As OPEC+ countries bring more oil to the market, Asian and European buyers are purchasing less U.S. light sweet crude, leading to price drops in the U.S. oil-producing regions.

Since April, OPEC+ (led by Saudi Arabia, Russia, and others) has added approximately 1.37 Mbpd to global supply, largely increasing its output, while still holding nearly 4.5 Mbpd in cuts. With more supply available, refiners in Europe and Asia have greater flexibility in sourcing crude. As a result, U.S. light sweet crude exports declined from 4 Mbpd in April to 3.8 Mbpd in May, and benchmark prices for WTI-Midland and Light Louisiana Sweet have dropped.

U.S. Light Sweet Crude Faces Fierce Competition

Expanding options from countries like Kazakhstan, Brazil, Libya, Algeria, and Norway have taken the favor in heavier crude-producing countries, pushing U.S. exports down. As a result, this sends light sweet grades (like U.S. shale) prices tumbling and dampens the competitiveness of U.S. crude.

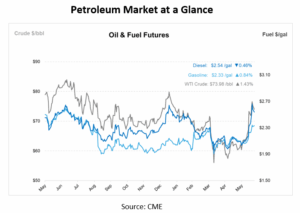

What does this look like? Prices for crudes like WTI-Midland, a major sweet grade from the U.S. shale region, have dropped largely by 45% since early March to just a 60-cent premium over U.S. crude futures. Over the same timeframe, Light Louisiana Sweet from the U.S. Gulf Coast dropped around 30%, narrowing to a $2.70-per-barrel premium.

Structural Shift in Global Refining

Refineries across Europe and Asia now have more options when it comes to sourcing crude oil, due to rising supplies from OPEC+. During periods of heavy refinery maintenance, lighter crudes, like the light sweet grades from the U.S., will see less demand, while interest in medium and sour crudes stays strong. This is what causes the U.S. light sweet crude prices to fluctuate.

While light crudes are generally easier to refine, many OPEC+ refineries have upgraded their equipment to handle heavier, sour crudes, which can be more cost-effective and still produce quality fuels. As Asian refineries finish their turnaround cycles and European plants boost output for the summer, demand for medium-sour crude has increased, making it even tougher for U.S. light sweet crude to compete.

Looking Ahead

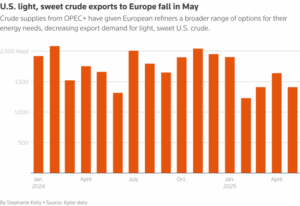

U.S. exports of light, sweet crude to Europe declined to 1.4 Mbpd in May, down from 1.6 Mbpd in April and 1.7 Mbpd in May 2024. Additionally, rig counts have fallen to their lowest levels since January, a signal that activity is being scaled back.

What does this mean for the U.S. oil industry? The pressure is increasing. Light sweet crude producers are facing tighter margins and a shrinking share of the global market. Unless domestic refineries ramp up demand or policy shifts occur, cuts to production and staffing are becoming increasingly likely. And for OPEC+ countries? They’re gaining the upper hand. The uptick in diverse crude streams gives them more leverage to negotiate favorable terms and refine oil at a lower cost. For crude oil buyers, the increased supply could mean more options and potentially stable or lower fuel prices. However, rising OPEC+ output may ultimately slow the transition away from fossil fuels, delaying progress toward cleaner energy goals.

Bottom Line

OPEC+ is increasing supply to regain market share from U.S. producers, which is putting downward pressure on crude prices, particularly for U.S. shale. As a result, major benchmarks like WTI-Midland and Light Louisiana Sweet have lost a portion of their premium value, while exports to Europe and Asia have declined. Refineries worldwide are shifting toward heavier and medium-sour crude grades, which are more cost-effective and better suited for fuel production — further weakening demand for U.S. light sweet crude. For U.S. producers, the impact could range from reduced drilling activity and output cuts to, if export losses persist, potential workforce reductions.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")