Week in Review: Crude Ticks Up on Geopolitics and Trade Optimism

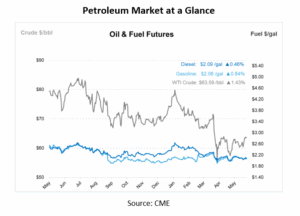

After two weeks of declines, oil markets jumped back up this week, with both Brent and WTI crude climbing. Brent crude finished the week up at around $65/bbl, while WTI rose to $63/bbl. The rally was driven by a mix of geopolitical tensions and renewed optimism in global trade, though underlying market shifts continue to pressure U.S. crude producers.

The week began with reports of a positive phone call between U.S. President Donald Trump and China’s President Xi Jinping. The leaders discussed rare earth exports and trade cooperation, and while no formal agreement was reached, markets responded to signs of resumed dialogue between the world’s two largest economies. Meanwhile, rising conflict between Russia and Ukraine—and Trump’s suggestion of potential sanctions on both nations if peace talks stall—added to the upward momentum in oil prices.

Macroeconomic data painted a mixed picture, adding complexity to the market. The U.S. trade deficit narrowed in April, prompting Goldman Sachs to revise its Q2 GDP estimate up to 3.7%. However, productivity declined, and unit labor costs rose significantly, adding inflationary pressures that could ripple into energy markets. Jobless claims also increased, though this may reflect seasonal volatility.

The true story behind price changes is tied closely to the types of crude on the market. Crude oil is generally classified as light or heavy based on its density, and sweet or sour based on its sulfur content. Light sweet crude—like the U.S. WTI-Midland—is easier to refine into gasoline and diesel and has traditionally been favored by refiners. However, as more refineries around the world are optimized to process heavier, sour grades, demand for U.S. light sweet crude is slipping.

That shift is becoming more apparent as OPEC+ ramps up production. Since April, the group—including Saudi Arabia and Russia—has added over 1.3 Mbpd to the market. These volumes, combined with growing exports from countries like Guyana, Brazil, and Kazakhstan, are giving refiners—especially in Europe and Asia—more options. Many are now choosing cheaper medium-sour grades over U.S. light sweet barrels. As a result, WTI-Midland’s price premium has fallen 45% since March, and Light Louisiana Sweet is down nearly 30%.

In May, U.S. crude exports fell to 3.8 Mbpd from 4 Mbpd in April. China, once a major buyer, avoided U.S. crude entirely for the second month in a row. And while Nigeria’s Dangote refinery doubled its U.S. crude intake year-over-year, it’s not enough to offset broader declines. With more competitively priced barrels flowing from the Middle East and other emerging producers, the US will have to find ways to keep pace.

Prices in Review

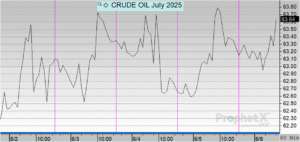

Crude prices opened at $61.11 on Monday and climbed steadily through midweek, reaching $63.36 on Wednesday. After a brief dip to $62.76 on Thursday, prices edged back up to $63.33 by Friday morning. Overall, crude gained $2.22 per barrel this week, marking a 3.63% increase.

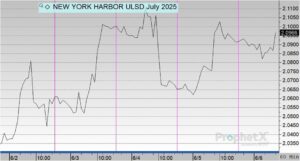

Diesel prices opened at $2.0038 on Monday and rose steadily through midweek, reaching a peak of $2.1032 on Wednesday. After a slight pullback to $2.0701 on Thursday, prices recovered modestly to $2.0945 by Friday morning. Overall, diesel prices increased by $0.0907 this week, representing a 4.53% gain.

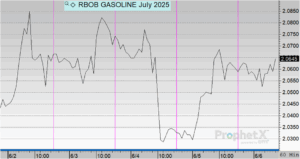

Gasoline prices opened at $2.0151 on Monday and climbed steadily through midweek, reaching a high of $2.0726 on Wednesday. After a brief dip to $2.0346 on Thursday, prices rose again to $2.0653 on Friday morning. Overall, gasoline gained $0.0502 this week, representing a 2.49% increase.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")