Week in Review: OPEC+ Holds Focus as Summer Demand Builds

Oil markets are trading down today, with WTI prompt crude futures ticking down about 56 cents per barrel and Brent crude down just shy of 30 cents per barrel. Markets are bracing for tomorrow’s OPEC+ meeting, where a decision on July production levels is expected. Kazakhstan’s Deputy Energy Minister hinted at a potential hike, though the scale remains uncertain. Meanwhile, Canadian crude prices rose in the Gulf Coast market as wildfires in Alberta threatened around 250,000 bpd of production, roughly 5% of Canada’s output.

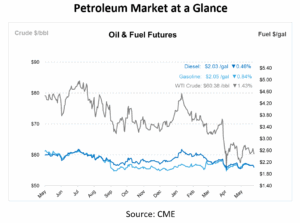

In the U.S., the EIA reported a larger-than-expected crude inventory draw of 2.8 million barrels last week, while gasoline and distillate stocks fell by 2.4 million and 0.7 million barrels, respectively. U.S. stockpiles remain below seasonal averages—crude by 6%, gasoline by 3%, and diesel by a profound 17%. The Jul25-Aug25 WTI prompt spread climbed to 74 cents, its highest since February, underscoring short-term supply tightness driven by refinery demand and supply constraints.

The upcoming OPEC+ meeting on May 31 has dominated headlines. The group is weighing whether to continue accelerating output increases, with a July hike of 411,000 bpd likely, mirroring recent increases in May and June. This strategy, led by Saudi Arabia and Russia, appears aimed at both regaining market share and applying pressure to overproducing members and U.S. shale producers. The group also agreed to establish a mechanism for setting 2027 production baselines, a move that could reshape future supply negotiations. While summer demand typically supports production increases, the window for further hikes could close beyond August unless global supply disruptions emerge.

OPEC+’s output strategy is already impacting U.S. shale producers. With WTI hovering near $60/bbl, drilling activity has slowed—rig counts have dropped, frac spread activity is down 28% year-over-year, and producers are delaying the completion of drilled wells. Despite the slowdown, overall U.S. output remains stable due to operational efficiencies and consolidation within the industry.

Broader economic indicators add to market complexity. U.S. GDP for Q1 was revised slightly higher to -0.2%, but consumer spending and real gross domestic income both declined, indicating underlying weakness. Weekly jobless claims also rose to 240,000, the highest level since 2021 for continuing claims. Still, the labor market remains resilient enough to support economic momentum with rising input costs and policy uncertainty.

On the geopolitical front, a U.S. court ruling temporarily blocked many of President Trump’s tariffs. However, the administration plans to appeal, and uncertainty around future trade policy remains high. Meanwhile, tighter U.S. sanctions on energy exports to China and potential new measures against Russia are fueling concerns about long-term crude flows.

With tightening inventories, slowing U.S. production, and anticipated summer demand growth outpacing supply by up to 700,000 barrels per day, bullish sentiment could take hold over the next few months. However, markets remain highly sensitive to policy shifts and geopolitical developments, with Saturday’s OPEC+ decision likely to set the tone for June and beyond.

Prices in Review

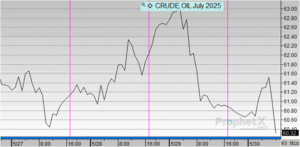

Crude prices opened at $61.70 on Tuesday following the Memorial Day holiday and saw modest fluctuations throughout the week. Prices dipped to $61.04 on Wednesday before increasing slightly to $61.83 on Thursday. However, the market dipped heading into the weekend, with crude opening at $60.94 on Friday.

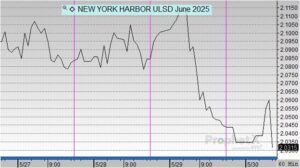

Diesel prices opened at $2.1113 on Tuesday after the Memorial Day holiday and declined steadily throughout the week. The sharpest drop occurred on Friday, with prices falling to $2.0448—the lowest point of the week. Midweek saw minor fluctuations, with prices reaching $2.0847 on Wednesday and $2.0870 on Thursday. Overall, diesel prices fell by $0.0665, marking a 3.15% decrease for the week.

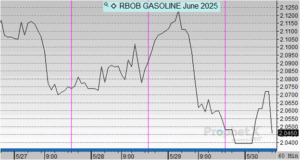

Gasoline prices opened at $2.1160 on Tuesday following the Memorial Day holiday and saw moderate declines through the week. The lowest point came on Friday, with prices slipping to $2.0517. After a midweek dip to $2.0730 on Wednesday, prices briefly jumped to $2.0910 on Thursday before continuing their downward trend. Overall, gasoline prices dropped by $0.0643, representing a 3.04% decrease for the week.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")