Week in Review – Oil Set for Weekly Gain Balancing Sanctions, Stimulus, and Surplus

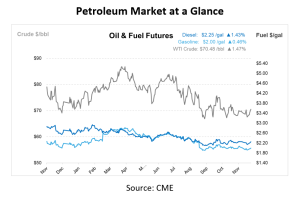

Oil prices rose over 1% today, marking their first weekly gain since late November, with WTI at $70/bbl, up over 3% for the week. Concerns about supply disruptions from tightened EU sanctions on Russia, potential U.S. actions, and China’s new stimulus measures pressured prices. The EU targeted Russia’s shadow tanker fleet with a 15th sanctions package, while Britain, France, and Germany warned of reactivating sanctions on Iran to prevent nuclear escalation.

China, the world’s largest crude importer, showed increased imports in November for the first time in seven months, driven by lower prices and stockpiling. This trend is expected to continue into 2025 as refiners benefit from favorable pricing and quotas. The IEA revised its 2025 oil demand growth forecast to 1.1 Mbpd, up from 990,000 bpd, supported by China’s economic measures, but a global supply surplus remains likely as non-OPEC+ nations are projected to boost output by 1.5 million bpd. Additionally, market sentiment is influenced by expectations of Federal Reserve rate cuts following signs of economic cooling in the U.S.

The Department of Energy’s weekly report revealed a mixed picture for energy markets. While crude inventories experienced a modest draw of 1.4 million barrels, including a 1.3 million barrel draw at Cushing, gasoline and distillate stocks surged with builds of 5.1 and 3.2 million barrels, respectively. Refinery utilization dropped by 0.9% to 92.4%, signaling slightly reduced production activity. Despite these bearish indicators, crude futures traded higher, potentially driven by external factors such as CPI data signaling inflationary pressures and news of tougher sanctions on Russia, which provided bullish momentum to the market.

The most significant concern lies in the days of supply for diesel fuel, which saw a two-day increase in the past week, a trend reminiscent of December 2024 when supply gained 10 days within weeks. This rapid buildup suggests higher production levels coinciding with softening demand, raising the risk of oversupply. If this trend persists, netbacks across markets could erode further, particularly through late December and early January. However, for those seeking to hedge against price volatility, this period may present an opportunity to lock in more favorable diesel prices before market dynamics shift. That said, any unexpected bullish developments, such as geopolitical events or unplanned supply disruptions, could quickly counteract this trend.

According to this week’s EIA Short-Term Energy Outlook, global oil production is set to grow by 1.6 Mbpd in 2025, with nearly 90% of this increase coming from non-OPEC countries. This follows OPEC+’s decision to delay planned production increases until April 2025.

In the U.S., crude oil net imports for 2024 have remained steady compared to 2023, as rising domestic production has matched increased refinery runs. However, in 2025, U.S. crude oil production is expected to continue growing while refinery runs decline, resulting in net imports falling to 1.9 Mbpd—the lowest annual level since 1971.

Prices in Review

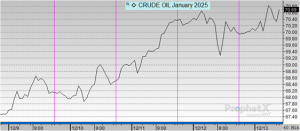

Crude opened the week at $67.15 before increasing each day. This morning, crude opened at $70.06, resulting in a $2.91 price jump for the week, or 4.33%.

Diesel opened at $2.1305 on Monday before climbing for the rest of the week. This morning, diesel opened at $2.2380, an overall increase of 10 cents or 5.04%.

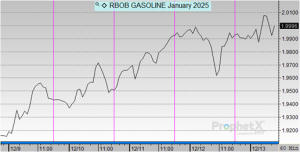

Gasoline opened the week at $1.9050 and saw steady gains throughout the week, trending similarly to crude and diesel. This morning, gasoline opened at $1.9905, an increase of 8 cents or 4.48%.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")