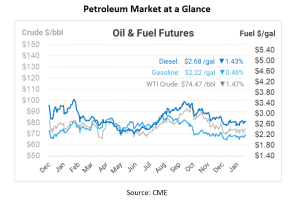

2024 Oil Landscape: Slower Demand, Surging Supply, and Lingering Challenges

Global oil demand is expected to see a significant slowdown in 2024, with the International Energy Agency (IEA) projecting a halving of the increase from 2.3 million barrels per day in 2023 to 1.2 million barrels per day this year. The agency attributed the reduction in growth to slowing oil demand in China, increased vehicle fleet efficiency, and the conclusion of pandemic recovery-related growth in 2023. Global liquid fuels production growth is also expected to slow, with OPEC+ maintaining production restraint and U.S. tight oil production growth decelerating.

In its latest oil market report (OMR), the IEA highlighted that the pace of demand growth outside of China notably slowed down in the second half of 2023, averaging around 300,000 barrels per day during that period. China is expected to continue leading oil demand growth in 2024, driven by its expanding petrochemical sector.

The global oil supply is projected to rise by 1.5 million barrels per day, reaching a new high of 103.5 million barrels per day in 2024. This growth will be dominated by the Americas, with the United States, Brazil, Guyana, and Canada contributing significantly, as they did in the previous year.

However, challenges persist in the oil market. Refineries on the US Gulf Coast are slowly recovering from the impacts of Winter Storm Gerri, which disrupted approximately 15% of the region’s crude processing capacity.

Additionally, the risk of disruptions in oil supply due to Middle East conflicts remains a concern, particularly for oil flows through the Red Sea and the Suez Canal. Recent airstrikes led by the US and UK on Houthi-controlled areas in Yemen have raised concerns of escalating conflict in the Middle East. This development has prompted commercial shipping networks in the region to divert tankers to longer routes, such as the Cape of Good Hope, to mitigate risks. As a result, freight rates for Europe-bound LR2 tankers have surged by 25% in just four days. The strikes, intended to weaken Houthi capabilities, come in response to ongoing attacks on US and UK ships, as well as international commercial shipping in key waterways like the Red Sea, Bab Al-Mandab Strait, and the Gulf of Aden. These actions follow earlier strikes and the designation of the Houthis as a global terrorist group by the US on January 17.

Russia’s seaborne crude shipments have also seen a decline, reaching a seven-week low due to bad weather at ports and the recent attack on a condensate processing facility near the Ust-Luga crude export terminal. The attack is the third on Russia’s large energy infrastructure facilities in the past week following drone assaults by Ukraine on an oil terminal in Russia’s second-largest city of St Petersburg and a storage facility in the town of Klintsy in the western Bryansk region.

In conclusion, the global oil market is expected to witness slower demand growth in 2024, marked by a significant reduction compared to the previous year. The market also grapples with challenges, including the gradual recovery of refineries from recent winter storms in the US and the persistent risk of disruptions in oil supply due to Middle East conflicts.

This article is part of Daily Market News & Insights

Tagged: 2024 Oil Landscape, Slower Demand, Surging Supply

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")