Week in Review- June 10, 2022

Today oil prices are up again as sweeping summer demand for gasoline and diesel are shaking up the market. This new peak summer demand has gasoline at nearly $5/gallon in all states as more and more people are hitting the road for vacation. This comes as yesterday oil prices were staying near 3-month highs as China imposed new lockdown restrictions in the financial hub of Shanghai due to the ongoing COVID-19 crisis.

The ease-up of restrictions in China saw a boost to exports in the month of May. China saw a near 17% jump in exports during May compared to the prior year. Factories are starting to restart, and facilities are filling up with workers as people start to resume their daily lives, a great sign for the supply and demand chain moving forward. However, parts of Shanghai are still imposing new restrictions to minimize new exposure risks associated with the virus.

This week Goldman Sachs said that this summer, retail gasoline prices must reach levels of $150-160 to help curb the menacing demand facing the United States. While strategists believe this is still a possibility for oil prices, there is still the unknown. The main thought from the investment group is that the worst is still yet to come for consumers, as once again on Tuesday gasoline reached a new record of $4.92/gallon. “We believe oil prices need to rally further to normalize the unsustainably low levels of global oil inventories, as well as OPEC and refining spare capacities,” Goldman Sachs strategists wrote.

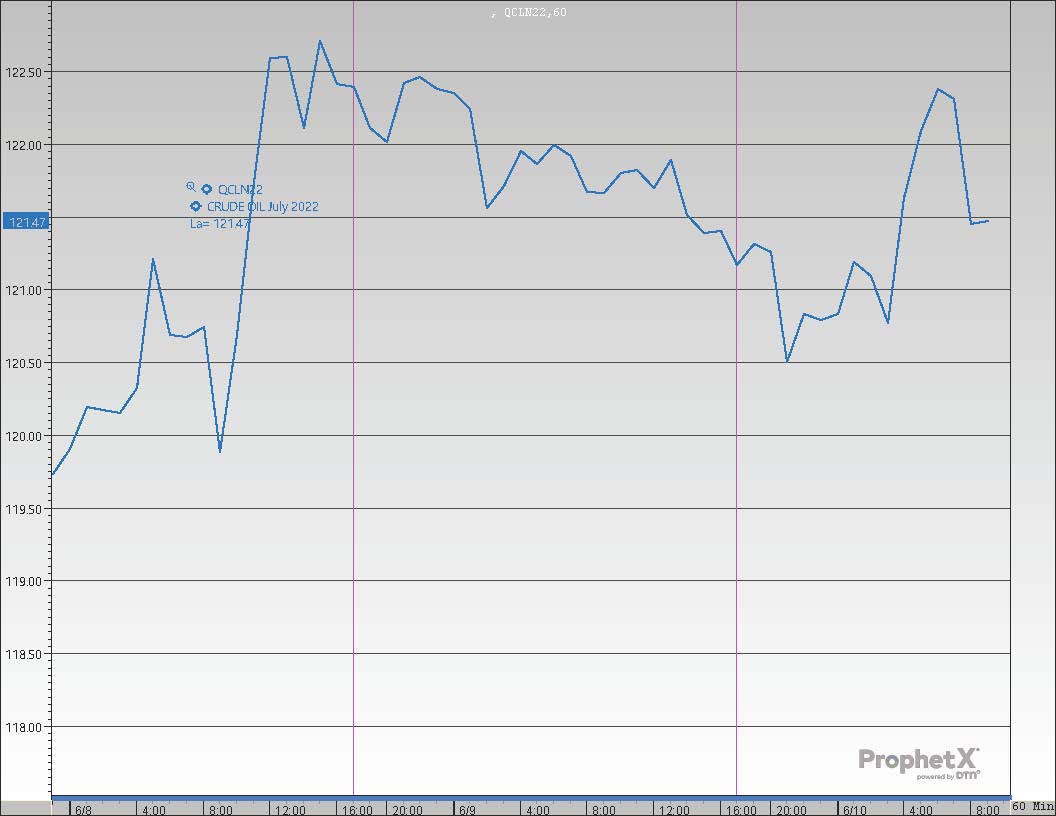

Lastly, on Monday crude prices were slightly up and hovering around the $120/bbl mark after falling following an OPEC+ supply deal. This deal saw Saudi Arabia raise their July prices after continued supply disruptions are still evident due to the Russian conflict in the East. Before the Saudis initiated this price increase, OPEC+ decided last week to boost their output for July and August by a total of 648,000 barrels per day. This increase was more than 50% of what was previously planned, impacting all OPEC+ members. The increase is also expected to offset some of Russia’s decline due to sanctions. One concern is that many of these countries have little room to increase their output, but OPEC+ is sticking with the current plan. These doubts about reaching the new output level caused crude oil to retreat from the $120 mark this morning before climbing slowly shortly after.

Crude Oil:

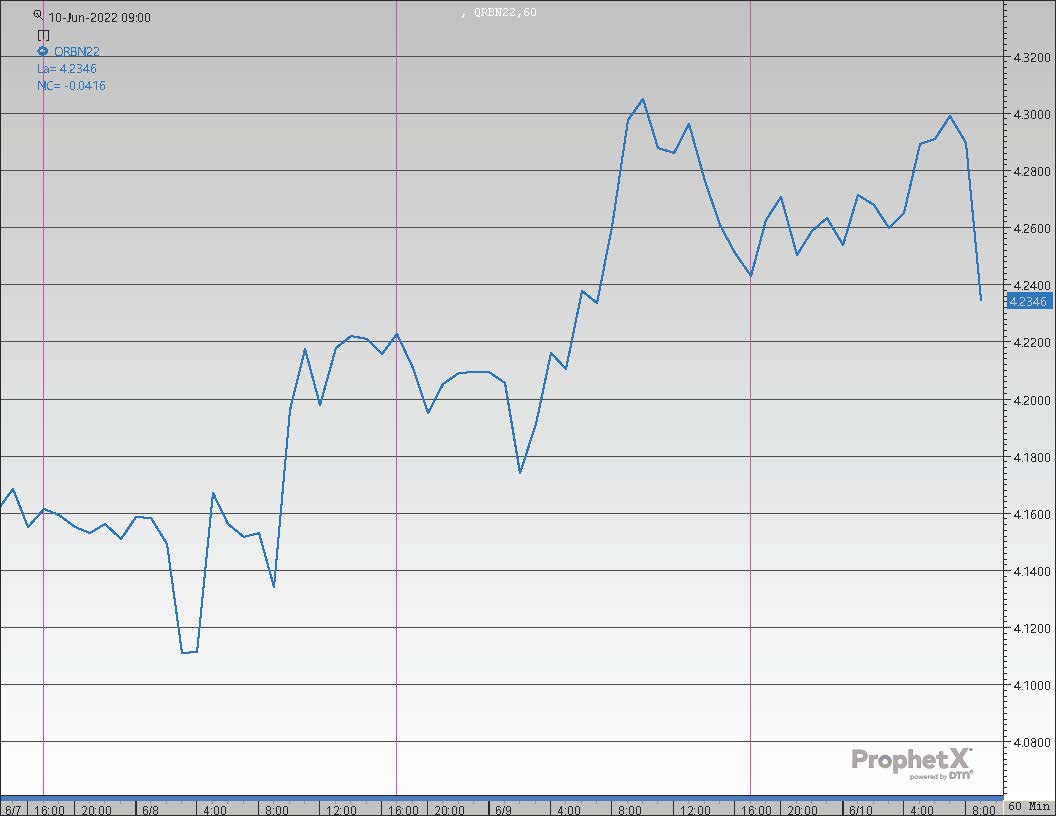

Diesel:

Gasoline:

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")