Week In Review – April 9, 2021

After several weeks of volatility, oil prices stabilized this week. Following Monday’s selloff, WTI crude prices consolidated to a narrow $1/bbl trading range.

The week began with OPEC+ agreeing to slowly increase its production, phasing in roughly 1 MMbpd of supply over the next three months. Saudi Arabia also announced it would cease its voluntary 1 MMbpd cuts next month. Oil markets took the news in stride – after an initial selloff, prices found their floor and settled in the middle of the $57-$63/bbl trading range we’ve seen over the past two months. The OPEC+ announcement was bearish for markets, but also suggests the group has more confidence in the global recovery than they did before.

Midweek, rumors began to circulate about the potential to return nearly 2 MMbpd of Iranian oil supply to global markets. The Biden administration is seeking to restart negotiations with Iran to lift sanctions and bring their nuclear program back under international supervision. So far, Iran has refused to begin talks until sanctions are lifted, but some informal talks have reportedly begun.

The EIA’s report on Wednesday brought mixed reactions – crude posted a surprise draw, but gasoline inventories rose far more than expected. America’s smooth vaccine rollout has boosted domestic consumption, supporting prices and giving international refiners a place to send their gasoline.

It’s still unclear what the future holds for fuel prices. Globally, COVID-19 cases are on the rise amid slow vaccine rollouts. Fortunately, the US – the biggest fuel consumer in the world – has been isolated from the new wave, so demand has been rising. There are still plenty of economic troubles at hand, reflected in the disappointing unemployment report this week. Between European demand weakness and the potential for Iranian oil supplies to hit global markets, a strong price break higher seems unlikely. On the other hand, if countries begin to get COVID under control, economic activity could flourish, unleashing a flood of demand that refiners are not ready to match.

This Week in Energy Prices

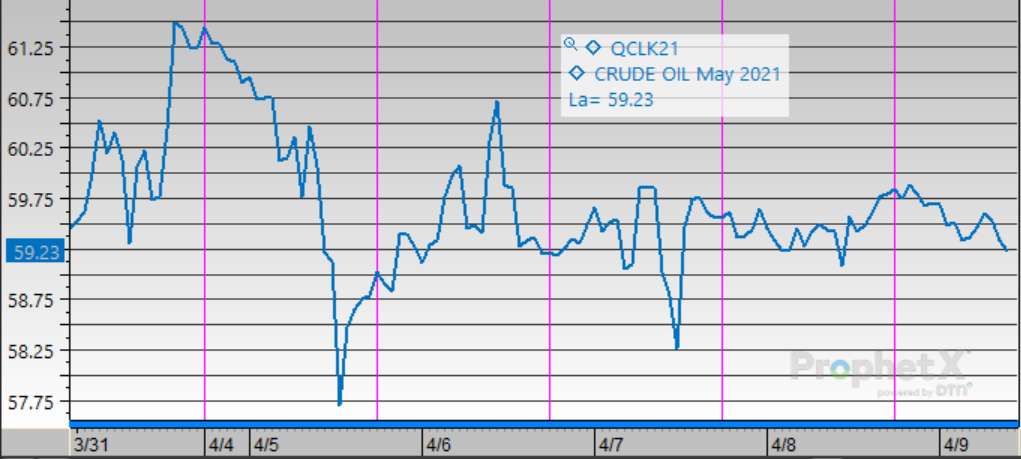

Crude prices began the week with a steep selloff caused by OPEC+ increasing output. Opening on Monday at $61.50, prices fell $3/bbl. But after that, prices stabilized around $59/bbl. This morning, crude opened that $59.76, a loss of $1.74 (2.8%).

Diesel prices followed crude markets through every peak and valley. After prices opened Monday at $1.83, they shed nearly 6 cents, then recovered a bit on Tuesday. This morning, diesel opened at $1.8079, down 2.2 cents (1.2%).

Gasoline saw the largest losses this week, caused by the large inventory build reported by the EIA. Gasoline opened the week strong, trading above $2/gal at $2.0214. They also saw a larger selloff on Monday, losing 6 cents. Unlike diesel, gasoline never recovered from its losses, instead falling even lower. On Friday morning, gasoline opened at $1.9598, down 6.2 cents (3.0%).

This article is part of Daily Market News & Insights

Tagged: Biden, biofuels, COVID, Dakota Access Pipeline, hurricane, renewable diesel

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")