Digging into Fuel Market Fundamentals

Oil prices are falling once more this morning, sinking close to the weekly lows set on Tuesday. Despite Wednesday’s bounce, oil prices have spent the rest of the week in the red as markets fear increasing production and sliding demand. Today’s article focuses on some of the on-going fundamental factors pushing oil lower.

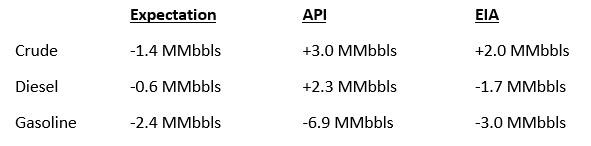

The EIA released their weekly data yesterday, a day delayed due to Labor Day. Crude inventories surprised markets with a build, though below the API’s earlier forecast. Both diesel and gasoline inventories fell due to severely lower refinery utilization.

Refiners ran at just 72% utilization last week due to on-going repercussions from Hurricane Laura, a 5% drop from the previous week. The worst is likely behind us on refinery utilization, but don’t expect a quick leap back to the 80% utilization seen a few weeks ago. 3:2:1 crack spreads (a refiner’s margin from turning crude into gasoline and diesel) have been just $8.50/bbl this week, compared to a historically normal range of $11-24 per barrel. Andy Milton, SVP of Mansfield Supply, commented on the refinery utilization and crack spreads:

“The big question ‘When will refinery utilization come back to healthier levels that may impact things like marine movements, netbacks, etc?’ Watch the gas inventory levels. If we continue seeing big declines in gas inventory levels and demand continues rising, we may see $13-$15/bbl type crack spreads by 1st quarter 2021 (a real breakout from current levels). The timing is important because the fall/early winter is, seasonally speaking, the lowest historical gas demand period. The market will want to entice gas production months ahead of the spring/summer driving season.”

On the demand front, the biggest source of concern was this week’s gasoline demand numbers, which continued its downward trend for a second week. Hitting 9.2 MMbpd two weeks ago (the highest since March), demand fell to 8.8 MMbpd last week and just 8.4 MMbpd this week. Demand is not only a million barrels per day below the seasonal average now, it’s also set to continue dropping.

US summer gas demand is a global phenomenon, supporting oil prices during the summer before consumers head inside to escape cooler weather. This year, summer demand never hit normal levels, and some fear winter demand will remain below trend. While diesel demand has performed relatively strongly – tracking the average seasonal level for the last several weeks – the dips in jet fuel and gasoline are weighing more heavily on markets. There just is not enough demand to sop up the products coming out of refineries.

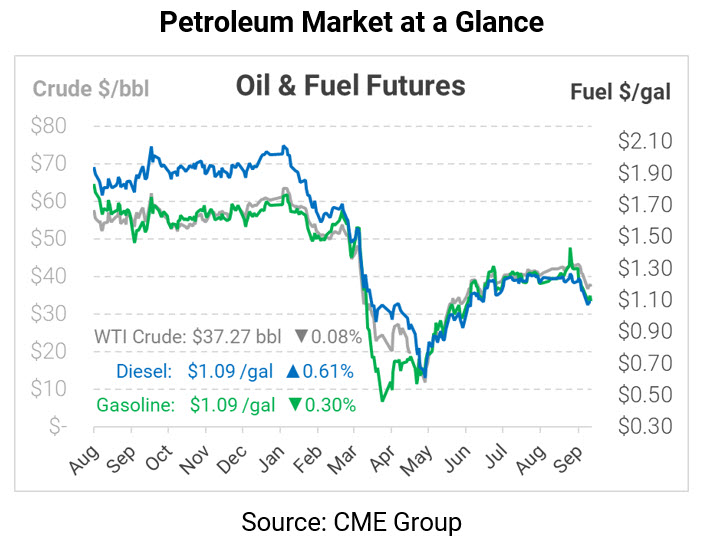

Crude prices are trading sideways this morning. WTI Crude is trading at $37.27, a loss of 3 cents.

Fuel is mixed in early trading this morning. Diesel is trading at $1.0890, a gain of 0.7 cents. Gasoline is trading at $1.0944, a loss of 0.3 cents.

This article is part of Daily Market News & Insights

Tagged: demand, eia, Refinery Utilization

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")