EIA Short-Term Energy Outlook: Petroleum Products

Petroleum Products

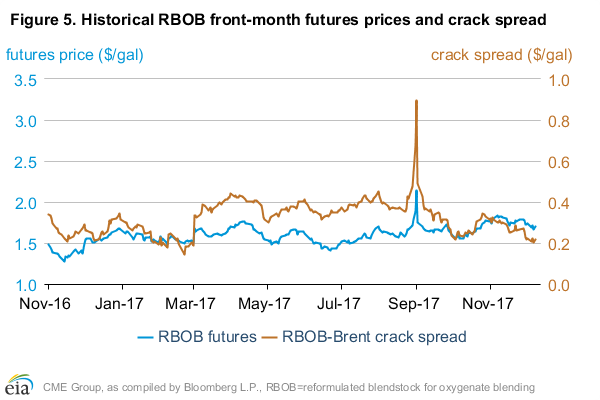

Gasoline prices: The front-month futures price of reformulated blendstock for oxygenate blending (RBOB, the petroleum component of gasoline used in many parts of the country) fell by 4 cents per gallon (gal) from November 1 to settle at $1.70/gal on December 7, 2017 (Figure 5). The RBOB-Brent crack spread (the difference between the price of RBOB and the price of Brent crude oil) fell by 8 cents/gal to settle at 22 cents/gal over the same period. EIA compares RBOB prices with Brent prices because EIA research indicates that U.S. gasoline prices usually move with Brent prices, the international crude oil benchmark.

Despite the decline in the gasoline crack spread towards the end of November 2017, the average gasoline crack spread set a five-year high for November. EIA estimates that U.S. gasoline consumption in November averaged almost 9.2 million barrels (b/d), which would be close to the five-year high for the month, if confirmed by EIA’s Petroleum Supply Monthly (PSM). Similarly, U.S. finished gasoline exports in the four weeks ending December 1 were more than 0.9 million b/d, which would set a five-year high for November.

Ultra-low sulfur diesel prices: The ultra-low sulfur diesel (ULSD) front-month futures price increased by 3 cents/gal from November 1 to settle at $1.90/gal on December 7, 2017. The ULSD-Brent crack spread (the difference between the price of ULSD and the price of Brent crude oil) declined by almost 1 cent/gal over the same period, settling at 42 cent/gal (Figure 6).

Distillate stocks as of December 1, 2017, were 0.7 million barrels lower than the five-year average. The total of distillate consumption and exports rose to 5.3 million b/d for the four weeks ending December 1, which would set a five-year high, if confirmed by the PSM. Because of lower distillate stocks and increased distillate demand this year, the ULSD crack spread has remained higher than its five-year average each month since July 2017 and has also remained significantly higher than the crack spreads in the second half of 2016.

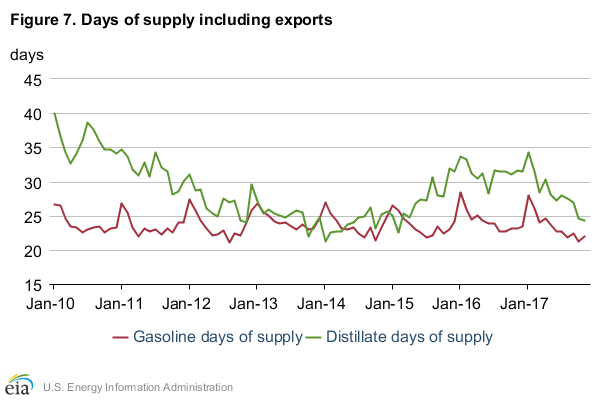

High demand for both gasoline and distillate resulted in each petroleum product’s days of supply in the U.S. market reaching the lowest levels in several years. When adding exports to product supplied in the traditional days of supply calculation, days of supply of total motor gasoline was 22 days as of the four weeks ending December 1, 2017 (Figure 7), slightly higher than the days of supply in October, which would have been the fewest days of supply since August 2012, if confirmed by the PSM. Similarly, days of supply of distillate fell to 24 days during the same period and would be the fewest days of supply since February 2015. The increasingly tight U.S. distillate market could make ULSD price increases more likely this winter if global demand for distillate remains high and if the United States experiences colder-than-normal temperatures in the U.S. East Coast, where heating oil is widely used for residential heating.

This article is part of Daily Market News & Insights

Tagged:

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.

(1)")

")