Week in Review – January 22, 2021

In the first few days of a new political administration, change is expected, and the Biden administration has not disappointed. President Biden has signed executive orders re-entering the US into the Paris Climate Accord, slowing pipelines, reinvigorating vehicle fuel efficiency targets, and issuing a 60-day ban on new drilling permits on federal land. Halting drilling permits will not stop existing drilling, nor will it upend the flurry of permits issued in the final days of the Trump administration. Some even say the 1,400 permits issued late last year could allow producers to continue operating for years, limiting the impact of any leasing ban imposed by Biden.

Although environmental regulations were an important part of Biden’s first week in office, they were dwarfed by the President’s proposals on financial stimulus and fighting the pandemic. Biden proposed a $1.9 trillion package to give money to consumers and provide a lifeline for schools and businesses. He also enacted the Defense Production Act to manufacturer vaccines faster. For now, these policies will have a bigger affect on oil markets than any specific policies related to the environment.

Early this week, the IEA released their monthly report, which downgraded Q1 2021 fuel demand by roughly half a million barrels per day. Although demand is still slightly bearish, the report pointed to OPEC+ austerity as a bullish factor that should provide support for the market until vaccines can bring a more long-term recovery. As new strains of COVID-19 begin popping up, new lockdowns are becoming necessary in different areas, so the vaccine can’t come soon enough.

Prices in Review

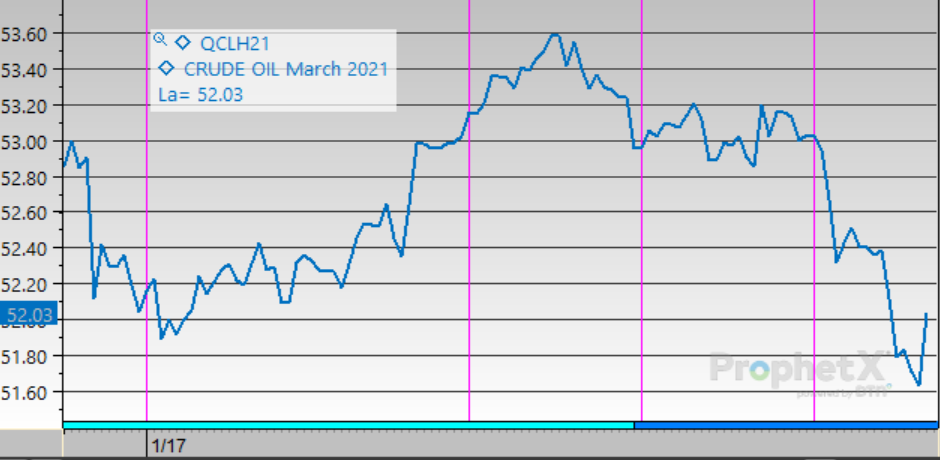

After a long holiday weekend, crude prices opened the week on Tuesday at $52.00/bbl, and for most of the week prices climbed. Hopes for more stimulus legislation loomed large, giving traders hope of better things to come. Prices peaked midweek near $53.50, retreating a bit later in the week. This morning, crude opened at $53.10, a gain of $1.10 for the week, though all of those gains have since been erased in morning trading.

Like crude oil, diesel prices moved higher mid-week before retreating. Diesel opened on Tuesday at $1.5842, climbing to a high of $1.61 before falling back. Diesel opened this morning at $1.6013, a gain of 1.7 cents for the week, but 3-cent losses are erasing all those gains this morning.

Gasoline was no exception for the week, peaking midweek and falling from there. Gasoline opened the week at $1.5181, and climbed throughout the week. The product opened at $1.5509 this morning, posting the largest gains (3.3 cents) for the week. Still, morning trading has wiped out those advances, putting gasoline back where it started for the week.

This article is part of Daily Market News & Insights

MARKET CONDITION REPORT - DISCLAIMER

The information contained herein is derived from sources believed to be reliable; however, this information is not guaranteed as to its accuracy or completeness. Furthermore, no responsibility is assumed for use of this material and no express or implied warranties or guarantees are made. This material and any view or comment expressed herein are provided for informational purposes only and should not be construed in any way as an inducement or recommendation to buy or sell products, commodity futures or options contracts.